All You Need to Know as a Canadian Investor Before Buying the Vanguard S&P 500 Index ETF (VFV)

Last Updated:

It often irks me to see people on Reddit advising new Canadian investors to "just buy the Vanguard S&P 500 Index ETF (VFV) and chill!" While VFV is undoubtedly a popular ETF, recommending it without a proper understanding of what it entails can lead to misguided decisions.

For many reasons, this approach may not be the best advice. I'm not criticizing VFV per se but investing in it without a clear understanding of its characteristics and implications could lead you to make hasty decisions, like panic selling, when you realize it's not exactly what you expected.

Before you consider investing a single dollar into VFV, it's crucial to arm yourself with a solid understanding of several fundamental aspects. Here’s my personal checklist to help you know exactly what you’re getting into with this ETF.

VFV: the basics

VFV tracks the S&P 500 Index, but there's a common misconception that this simply includes "the largest 500 US stocks"—actually, that definition better fits the Solactive 500 Index.

Instead, the S&P 500's constituents are chosen by a committee based on several criteria including float-adjusted market cap, trading volume, earnings, and their prominence in the economy, making it somewhat more actively curated than many assume.

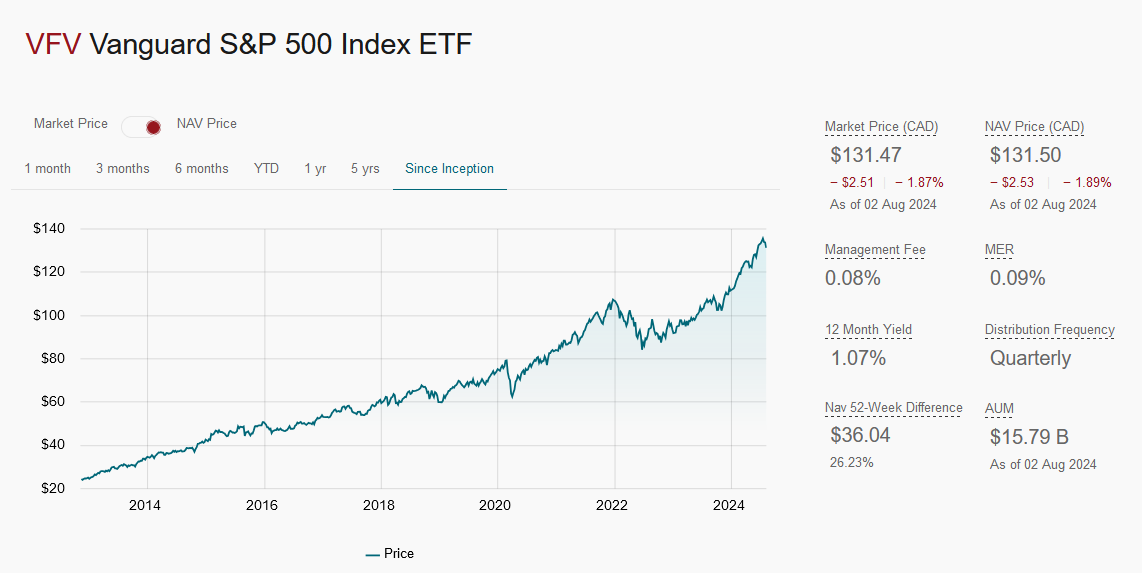

VFV itself is an index ETF that replicates the constituents of the S&P 500 by buying and holding them in the same proportions. However, there's a simplifying catch: VFV primarily holds a U.S. S&P 500 ETF, specifically VOO.

This means when you buy VFV in Canadian dollars, Vanguard Canada converts your CAD to USD at institutional rates and purchases shares of VOO. For this service, you pay a management expense ratio of 0.09%, which includes VOO's 0.03% MER.

Understanding this structure is crucial because it introduces two main mechanics that affect your investment, which we'll explore next.

VFV: foreign exchange risk

If you're holding VFV in CAD but it holds VOO in USD, you're exposed to foreign exchange rates, which can significantly affect your returns. This is known as currency risk and can manifest in two ways:

- USD appreciates against CAD: If the USD strengthens relative to the CAD, then all else being equal, the price of VFV would rise. This is because the underlying assets (VOO shares), denominated in USD, become more valuable in CAD terms.

- CAD appreciates versus USD: Conversely, if the CAD strengthens against the USD, the price of VFV would fall, all else being equal. This decrease occurs because the value of the underlying USD assets would be lower when converted back to CAD.

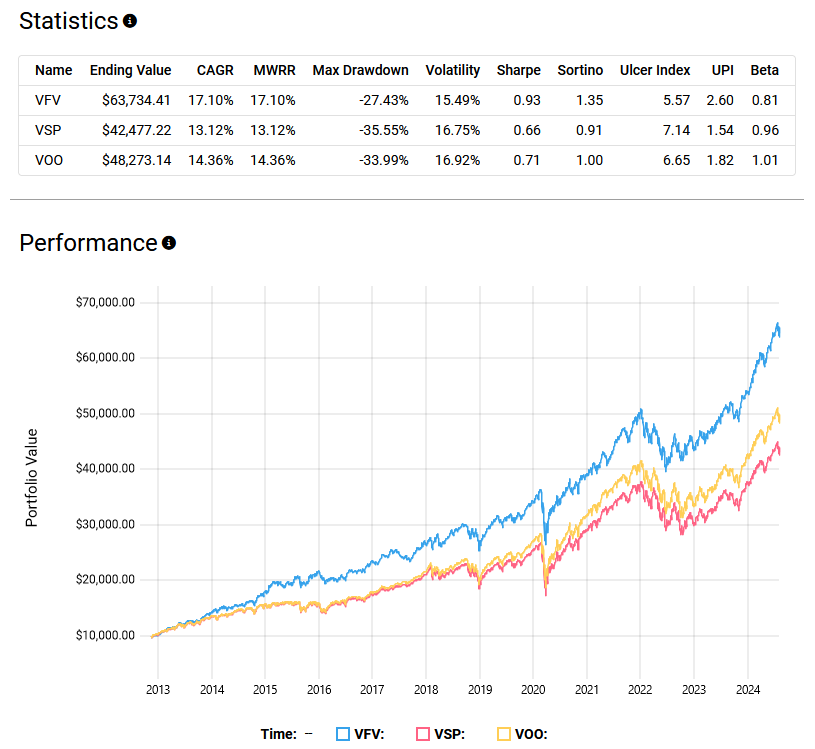

Historically, this currency risk has worked in VFV's favor. The rising USD over the last decade has helped VFV strongly outperform its CAD-hedged counterpart, VSP, which uses derivatives to neutralize this currency effect. This can be seen in the performance comparison chart below.

So, which is better now? With the USD still currently high, you might be tempted to opt for VSP to avoid currency risk. However, switching to a hedged ETF based on current currency strength could be seen as a form of market timing. If you were capable of accurately predicting FX movements, you might as well trade forex directly.

The key takeaway here is to expect VFV's performance to deviate from the actual S&P 500 index on a daily basis, for better or worse, depending on the USD-CAD exchange rate relationship.

VFV: withholding tax

As a Canadian investor purchasing U.S. stocks, you'll encounter a withholding tax—Uncle Sam withholds 15% of your dividends in most scenarios, and this applies even if you hold these investments in a TFSA.

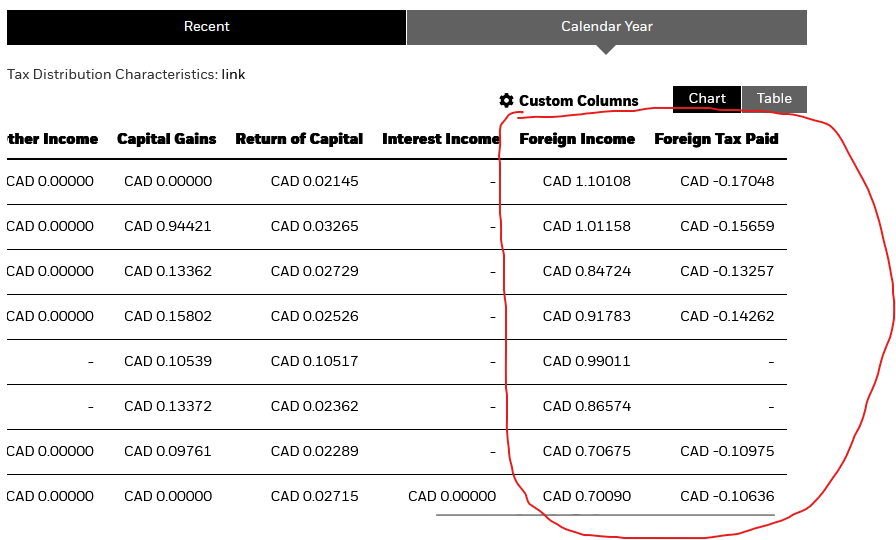

This withholding tax also affects ETFs like VFV. Remember, VFV holds VOO. When VOO pays a dividend to VFV, it's docked 15% before VFV passes what's left to you.

Annoyingly, Vanguard doesn't make this withholding tax situation very clear on their website, unlike BlackRock, which does a better job with their iShares Core S&P 500 Index ETF (XUS), providing a detailed table showing how much was withheld each quarter.

This 15% withholding on foreign-sourced income is unavoidable if you hold VFV. Each quarter when it pays a distribution, 15% of the dividend income is withheld.

While this might seem minor, it does add some drag to your returns. Considering VOO's 30-day SEC yield of 1.26%, the tax drag is about 0.19% per year. This should be considered in addition to your 0.09% MER for a more accurate total cost of ownership.

If you're looking to avoid this tax, one option is to buy and hold a U.S. ETF like VOO in an RRSP, where it's exempt from foreign withholding tax. However, the currency conversion costs imposed by your brokerage could offset this benefit.

For instance, Wealthsimple charges a 1.5% currency conversion fee. The only workaround I've found is to be a premium user with a USD account, which requires having $100,000 in assets, and linking a USD bank account for deposits—this works well if most of your income is in U.S. dollars.

If your goal is to buy and hold VOO directly, my recommendation is to use Interactive Brokers, which charges the lowest FX rates and allows conversion at spot prices. Doing this within an RRSP enables you to retain all of VOO's dividends without the deduction of withholding taxes.