VistaShares Target 15™ Berkshire Select Income ETF (OMAH) Review

Last Updated:

Berkshire Hathaway just held its first annual general meeting without Warren Buffett. It is hard to imagine Berkshire being quite the same without Buffett at the helm. At 95, succession has shifted from a distant question to a present reality.

Now, the new CEO Greg Abel has been publicly endorsed by Buffett and has spent years inside the Berkshire system being mentored. He understands the culture, the capital allocation philosophy, and the long-term, owner-operator mindset that built the company.

For those less familiar, Berkshire Hathaway is one of the most diversified holding companies in the world. At its core is a capital allocation flywheel. Insurance operations from GEICO generate float, which Berkshire then deploys as low-cost leverage across wholly owned businesses and investments.

That includes cash-generating private subsidiaries such as BNSF Railway, Duracell, and Berkshire Hathaway Energy, along with smaller but still profitable operations like See's Candies.

Then there is the public equity portfolio. That is the part most investors pay attention to, especially through Berkshire’s 13-F filings. Over the years, Buffett has built large positions in companies like Apple, Bank of America, Coca-Cola, and American Express to name a few.

When you invest in Berkshire, you get all of it. The insurance engine, the private businesses, the public equities, and the top-tier capital allocation decisions that tie everything together.

But not everyone wants that full package. Some investors are specifically interested in the public equity sleeve. Until recently, there was no simple way to isolate that exposure in a single product.

That changed with the launch of the VistaShares Target 15™ Berkshire Select Income ETF (OMAH) in May 2025. The pitch is straightforward: provide exposure to Berkshire’s public stock holdings and layer on options to generate yield. The headline number is a 15% annual income target, paid monthly.

That is notable because Berkshire itself does not pay dividends. Buffett has long argued that retaining earnings and reinvesting internally is a more efficient way to compound capital. Dividends tend to come from companies that lack high-return reinvestment opportunities above their cost of capital.

OMAH offers a different path. Instead of relying on Berkshire to distribute income, it attempts to manufacture it through derivatives. That can be appealing if you want cash flow tied to Berkshire’s holdings without having to buy 100 shares of Berkshire Hathaway Class B and sell covered calls.

But as with any income-focused ETF, especially one targeting a double-digit yield, there are trade-offs. Here is how OMAH stacks up so far in my opinion.

OMAH: What I Like

OMAH’s portfolio does a solid job replicating Berkshire’s public equity holdings. There are some differences in weight since this is an active strategy, but the core names are all there. If you like Berkshire’s public portfolio, you are getting a fairly faithful version of it here.

OMAH investors still get meaningful exposure to Berkshire Hathaway itself at around 9% as the second-largest holding, along with the usual heavyweights like Apple, American Express, Occidental Petroleum, Alphabet, Coca-Cola, Bank of America, Chevron, and Moody's to name a few.

Source: VistaShares as of May 4th, 2026

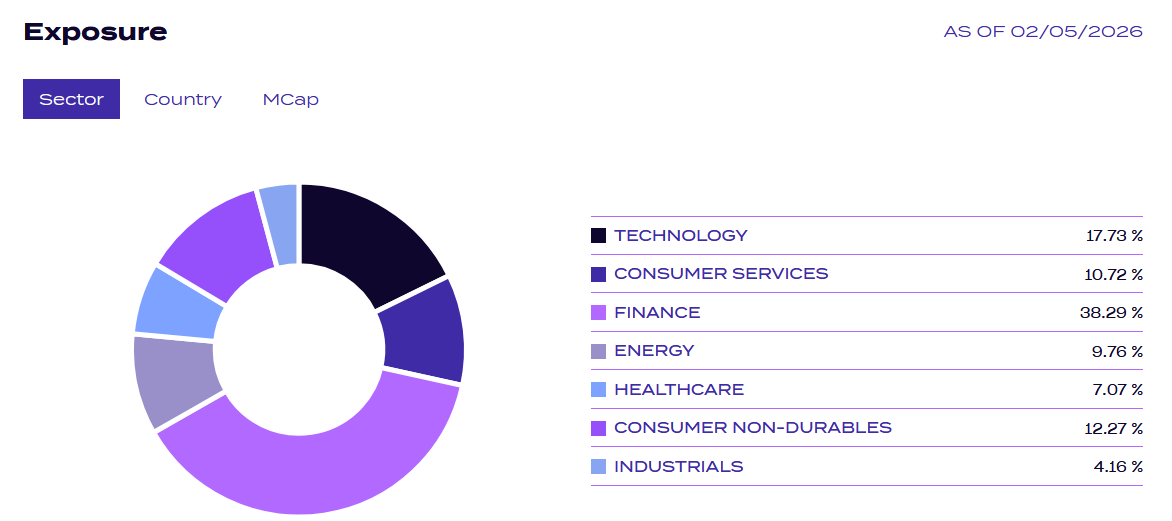

Sector exposure also looks very “Berkshire.” There is still a heavy tilt toward financials and consumer-facing businesses, which aligns with Buffett’s long-standing circle of competence. At the same time, there has been a gradual increase in technology exposure, which reflects how the portfolio has evolved.

Source: VistaShares as of May 4th, 2026

What will draw most investors, though, is the options overlay. OMAH primarily generates income through covered calls. You sell call options on stocks you already own, collect a premium, and in exchange, give up some upside beyond a certain price. The size of that premium depends on factors like implied volatility, time to expiry, and how far the strike price is from the current market price.

One thing I do like here is that OMAH sells options on individual stocks rather than broad indexes. That gives the managers more flexibility. Instead of mechanically selling calls on the entire portfolio every month, they can adjust strike prices, expiries, and coverage levels based on individual names.

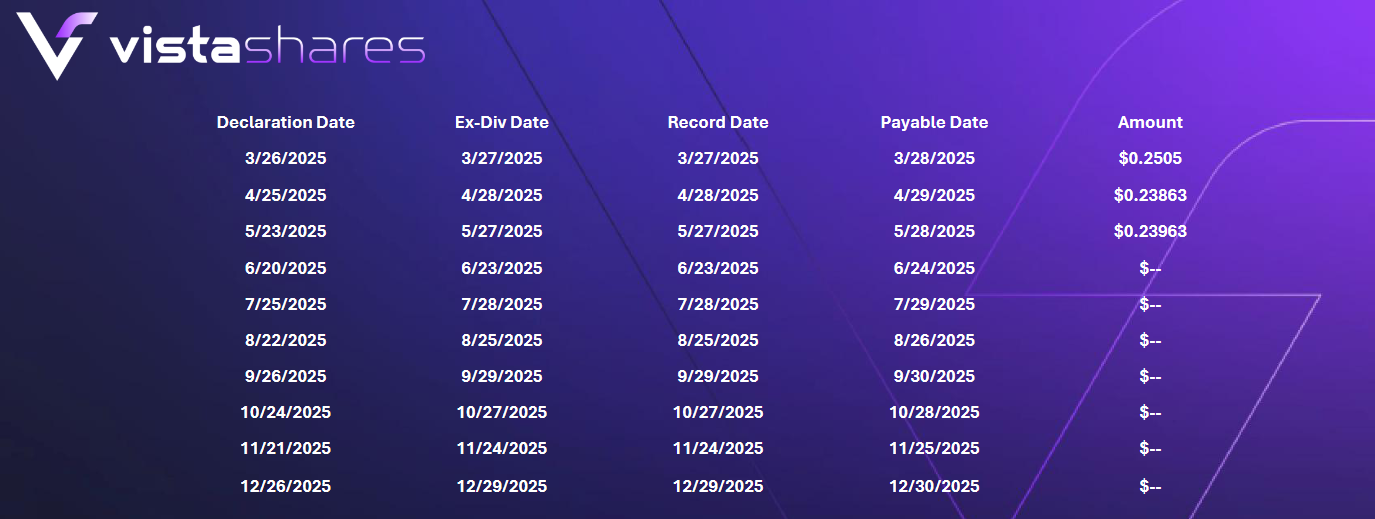

On the income side, the 15% figure is a target, not a guaranteed yield. OMAH targets a 1.25% monthly yield. Multiply by 12 months in a year, and you get the 15% target income.

Source: VistaShares as of May 4th, 2026

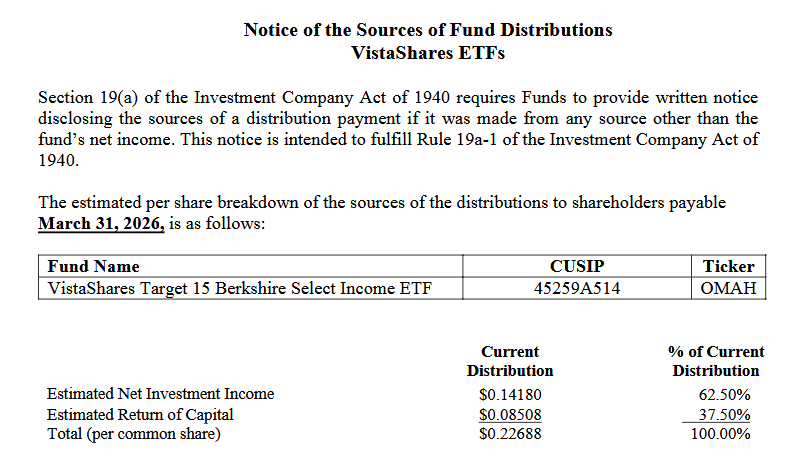

Distributions can come from option premiums, dividends, capital gains, interest, and return of capital, which occurs when distributions are paid in excess of the ETF’s current and accumulated earnings and profits. That last component tends to get criticized, but it is not inherently a negative.

Return of capital is not immediately taxable and instead reduces your adjusted cost base, deferring taxes until you sell. Based on the 19a-1 notice, about 37.5% of the most recent monthly distribution is estimated return of capital. That figure can change throughout the year, and the final breakdown is only confirmed at year-end on the form 1099-DIV.

Source: VistaShares as of May 4th, 2026

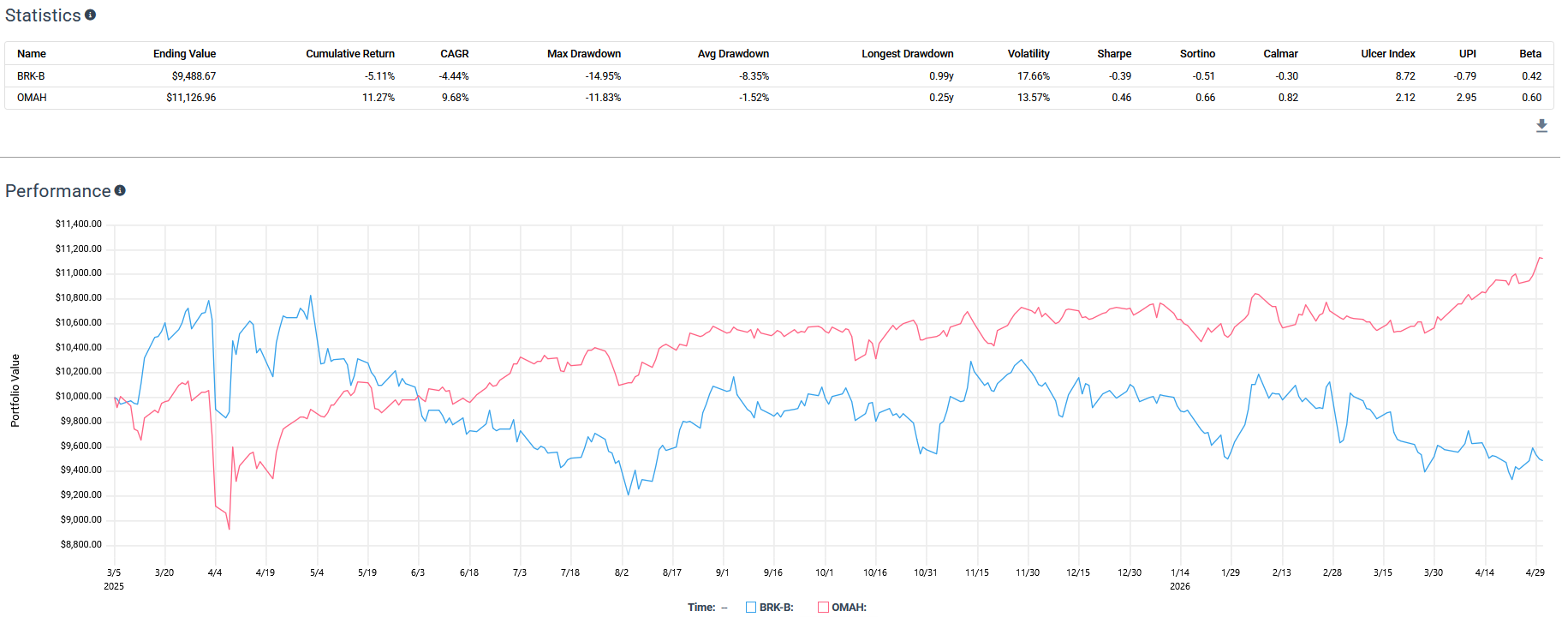

So far, performance has held up reasonably well. Since inception, OMAH has delivered a 9.68% annualized return, while Berkshire Hathaway Class B has declined by about 4.44% over the same period.

Source: Testfolio.io as of May 4th, 2026

That is a short time frame, so it does not prove much, but it is a better start than many double-digit derivative income ETFs that have seen steady net asset value erosion.

OMAH: What I Dislike

No ETF is perfect, and with OMAH there are a few things here I would have liked to see handled differently. The first is the 15% income target.

It is a nice, clean number, but it is also very ambitious. Many of Berkshire’s holdings are lower-volatility businesses. Lower volatility generally means lower option premiums. In a calmer market, it becomes harder to generate that level of income without leaning more heavily on return of capital.

Personally, I think more conservative target, closer to 12%, would likely be easier to sustain over time without relying on excessive return of capital. This minimizes the risk of NAV erosion.

The second issue is cost. OMAH charges a 0.95% expense ratio. That is very high and close to leveraged ETF levels. Active management and options strategies do cost more, but this is still a meaningful drag. On a $10,000 investment, that is about $95 per year in fees.

In my opinion, bringing that down closer to 0.75% would make it much more competitive with other actively managed income ETFs, especially given OMAH’s current scale at $747.41 million in assets.

OMAH: My Verdict

I would give OMAH a 7/10. The ETF does a good job replicating Berkshire’s public equity portfolio. The options overlay is thoughtfully implemented, with flexibility around individual positions rather than a rigid, index-level approach. And early performance has been decent, at least relative to Berkshire itself.

What holds it back are the trade-offs. The 15% income target may be difficult to sustain without relying more heavily on return of capital, and the 0.95% expense ratio is higher than I would like to see.

It is also worth repeating that the income from ETFs like OMAH is not free money. On the ex-distribution date, the fund’s net asset value drops by the amount of the payout. That is just how the math works.

If you are not actively drawing income from your portfolio, this type of ETF may not make much sense. You are effectively paying fees to receive distributions, some of which may be your own capital, and then potentially reinvesting it after the drag from taxes.

If your goal is long-term capital appreciation, a lower-cost index ETF or simply owning shares of Berkshire Hathaway may be the more straightforward approach. But if you want income and like the Berkshire portfolio, OMAH is one of the more direct ways to get there.