iShares Core High Dividend ETF (HDV) 2024 ETF Review

Last Updated:

Nearly all the major asset managers—State Street, Vanguard, Schwab, and iShares—offer a lineup of dividend-focused ETFs. These usually include a mix of high-yield options for income seekers and dividend growth funds for those prioritizing long-term appreciation.

For iShares, the high-yield option for U.S. markets is the iShares Core High Dividend ETF (HDV). The “core” in its name signals that it’s part of iShares’ low-cost “portfolio building block” lineup, designed to be an affordable staple for investors building diversified portfolios.

However, a slick name and strong marketing alone aren’t enough reason to invest. Here’s my critical analysis of how HDV measures up as a high-yield dividend ETF.

HDV: What I like

One of HDV’s biggest strengths is its scale. With $11.5 billion in assets under management (AUM), this ETF is well-capitalized and not at risk of shutting down anytime soon. Its focus on U.S. equities, combined with its large AUM, also translates into excellent liquidity. The fund boasts a 30-day median bid-ask spread of just 0.02%, making it easy and cost-effective to trade.

As part of iShares’ Core lineup, HDV is designed to be a low-cost portfolio building block. Its expense ratio is just 0.08%, or $8 annually for every $10,000 invested, which is highly competitive for a high-yield dividend fund.

HDV tracks the Morningstar Dividend Yield Focus Index, a benchmark that applies rigorous screening criteria. It selects stocks based on Morningstar’s Economic Moat Rating (to identify companies with sustainable competitive advantages), Uncertainty Rating (which measures the projected dispersion of fair value estimates), and Distance to Default Score (an assessment of volatility and leverage).

The fund is also fairly tax-efficient, as it excludes real estate investment trusts (REITs) to ensure all dividends qualify as “qualified income” under U.S. tax law. At the same time, it offers a decent 30-day SEC yield of 3.56%, providing an attractive income stream for dividend-focused investors.

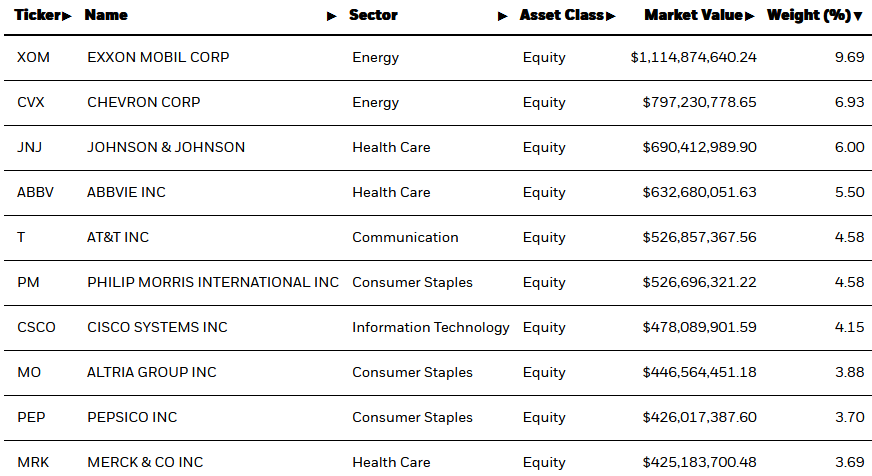

HDV holds a portfolio of 75 stocks, featuring many familiar blue-chip names across sectors like energy, healthcare, and consumer staples. Stocks are weighted by their 12-month dividend payment. This provides diversified exposure to some of the most stable blue-chip dividend payers in the U.S.

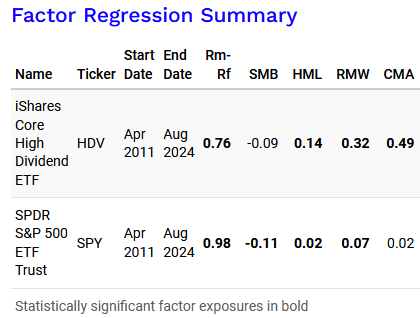

As expected, HDV also shows favorable factor loadings, particularly for value (HML), profitability (RMW), and investment (CMA). These mean that, on average, HDV’s holdings tend to be undervalued, highly profitable, and conservative with their capital investments

HDV: What I dislike

While HDV has some strong points, there’s plenty to criticize about the fund as well. The focus on high-yield stocks has its merits, but several structural issues weigh heavily on its performance.

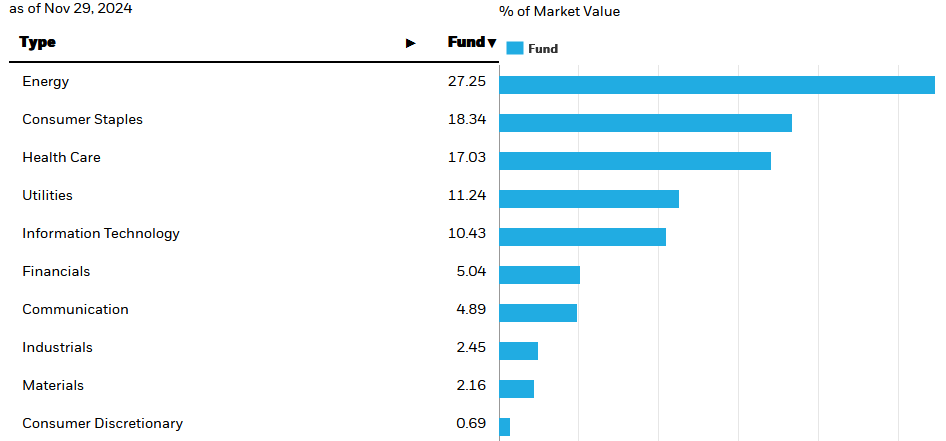

First, it lacks sector or security caps, leading to some unusual and potentially risky overweights. For instance, HDV currently allocates 27% of its portfolio to the energy sector.

This overweight worked out well in 2022 during a period of high inflation and rising energy prices, but it’s likely to introduce significant volatility in other market conditions. For comparison, the S&P 500 allocates just 3.44% to energy—HDV overweights it more than sevenfold.

The Morningstar Dividend Yield Focus Index, while theoretically sound, also has transparency issues. Its criteria, such as the Economic Moat Rating and Uncertainty Rating, are subject to a fair amount of subjectivity.

Morningstar is a highly reputable source, but investors can’t dig into the methodology behind these ratings as deeply as they could with other index ETFs. This lack of transparency makes HDV’s underlying strategy inherently harder to evaluate.

Another issue lies in HDV’s portfolio management. The fund undergoes quarterly reconstitution and rebalancing, which is an unusually frequent schedule. To clarify, rebalancing adjusts the weights of existing holdings to match the index’s rules, while reconstitution adds or removes stocks from the portfolio.

Most ETFs follow a more typical cadence of quarterly rebalancing and annual reconstitution. The combination of both happening quarterly in HDV results in a high annual turnover rate of 67%.

This turnover isn’t a capital gains issue since ETFs use in-kind creation/redemption to avoid distributions, but it severely curtails HDV’s ability to let winners run. Instead, holdings are frequently adjusted or swapped out, limiting their long-term growth potential.

I suspect this is one of the reasons HDV has underperformed over time. In a backtest from March 31, 2011, to November 29, 2024, HDV delivered a total return of 10.39%, significantly lagging the SPDR S&P 500 ETF (SPY), which returned 13.77% over the same period.

HDV: My verdict

HDV scores a 6.5/10 for me. It’s still above average as dividend ETFs go (and believe me, there are some shockingly senseless ones out there), but you can definitely find better options.

I like its low expense ratio, above-average yield consisting solely of qualified dividends, and its focus on large-cap, blue-chip companies. The fund also provides good exposure to somewhat undervalued, high-quality stocks, which aligns well with its high-yield strategy.

However, there are clear downsides. The index methodology feels like a black box, offering less transparency than other ETFs. The quarterly reconstitution creates high turnover, preventing the fund from letting winners run.

Its sector overweights, such as the 27% allocation to energy, add unnecessary volatility. With just 75 U.S. large-cap stocks in the portfolio, it also feels more limited compared to broader, more diversified options.