Middlefield Real Estate Dividend ETF (MREL): The Good, The Bad, and The Ugly

Last Updated:

By and large, I am not really a fan of Canadian ETFs that invest primarily in real estate investment trusts, or REITs. Part of that comes down to the structure of the Canadian REIT market itself.

It is a relatively small universe, and with commission-free brokerages like Wealthsimple now widely available, it is not particularly difficult for investors to assemble their own basket of REITs and avoid paying an ongoing management expense ratio, or MER.And on that note, this is one corner of the Canadian ETF market where fees have for the most part, stubbornly refused to come down.

Even many of the older passive index-tracking REIT ETFs continue to charge fees that I would consider prohibitively expensive. Maybe those expense ratios made sense when these products first launched around the turn of the 21st century. Back then, ETFs themselves were still a novelty and the alternatives were often active mutual funds charging well over 1%.

In 2026, though, the landscape looks very different. Assets under management have exploded. Competition has increased. Trading commissions have largely disappeared. Yet many Canadian REIT ETFs still charge investors what I consider a hefty fee for what is ultimately a straightforward benchmark.

That said, not all REIT ETFs are passive. One actively managed option that I actually have a bit of a soft spot for is the Middlefield Real Estate Dividend ETF (MREL). It is notable because it is managed directly by Middlefield president and CEO Dean Orrico.

Now, I do not usually write ETF reviews focused on individual Canadian funds. There are simply too many products and not enough hours in the day. But I am making an exception for MREL because I think it is one of those ETFs that investors are either going to love or hate.

Personally, I really want to love it. There are several things this ETF does well, but there are also a few things that hold it back from being an easy recommendation. To be clear, none of these are fatal flaws. In fact, as you'll see shortly, there is plenty to like about MREL. I simply think that any ETF review should present both sides of the story.

So, before the Middlefield faithful grab their pitchforks, hear me out. These are just my opinions as someone who spends far too much time looking at ETF portfolios, fee structures, and performance data. You may ultimately come to a different conclusion, and that's perfectly fine.

MREL: The Good

The good is admittedly backward-looking, and I always like to start these discussions with the same disclaimer: past performance does not predict future results. Still, credit is due where credit is warranted: MREL has performed exceptionally well relative to its peers.

The fund earned a FundGrade A+ Award for 2025, an annual designation awarded to Canadian investment funds that have demonstrated strong risk-adjusted performance within their categories. It also currently carries a five-star Morningstar rating, placing it among the top performers in a peer group of 107 real estate funds based on historical risk-adjusted returns.

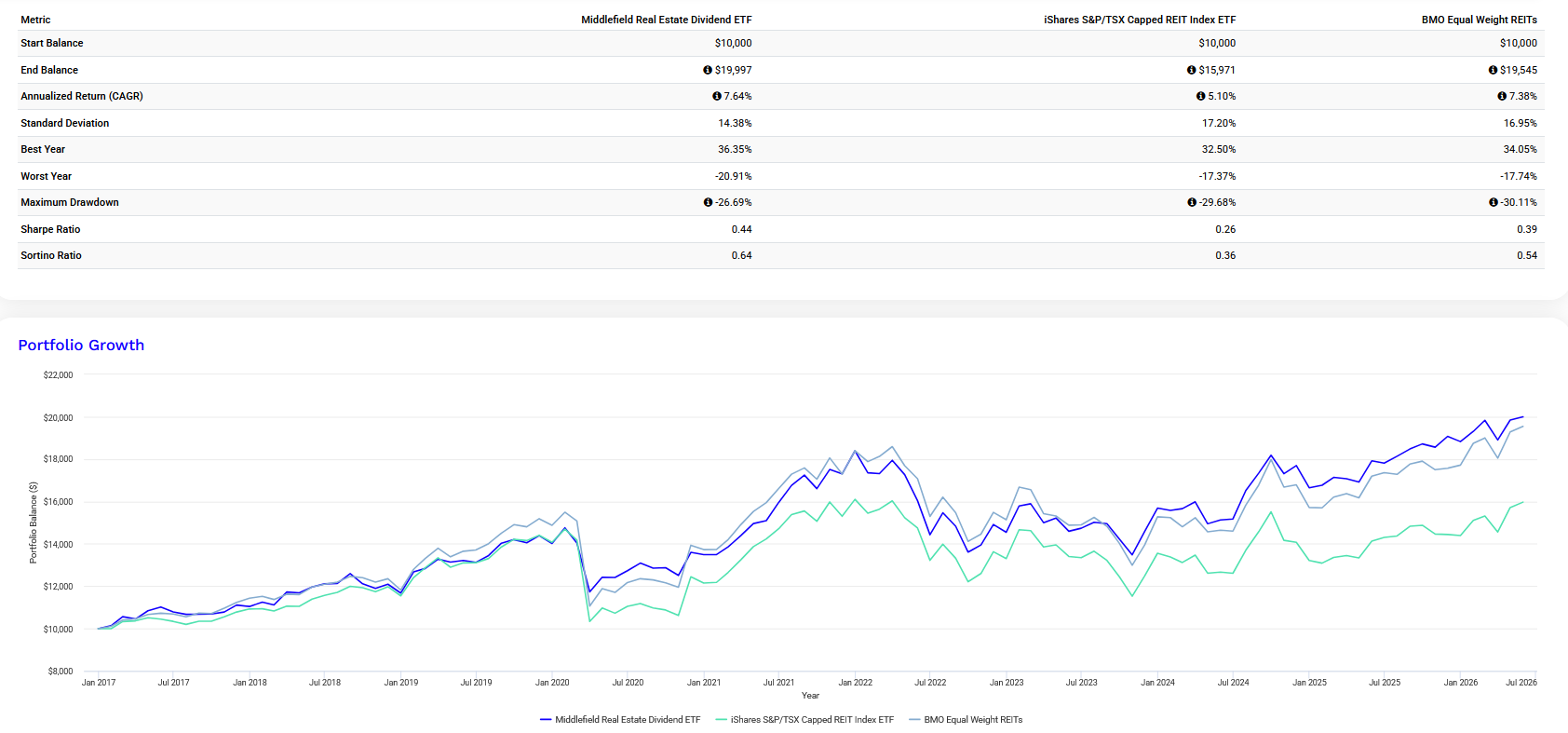

To get a better sense of how MREL has stacked up against its competitors, I ran a backtest from January 2017 through May 2026 using Portfolio Visualizer. I compared it against two of the most popular Canadian REIT ETF options available: the market-cap-weighted iShares S&P/TSX Capped REIT Index ETF (XRE) and the equal-weighted BMO Equal Weight REITs Index ETF (ZRE).

The results were impressive. Over the period, MREL delivered a 7.64% annualized total return. That compares to 5.10% for XRE and 7.38% for ZRE. More importantly, MREL achieved those returns while exhibiting lower volatility and a shallower maximum drawdown. The end result was substantially better risk-adjusted performance: MREL generated a Sharpe ratio of 0.44 versus 0.26 for XRE and 0.39 for ZRE.

Source: Portfolio Visualizer

Part of this highlights something I've long believed about real estate investing: REITs are one of those asset classes, similar to fixed income, where active management can occasionally justify its existence. The underlying securities are generally less liquid than large-cap equities. Analyst coverage is often thinner. Property markets themselves are highly segmented.

MREL's portfolio absolutely takes advantage of that flexibility. One of the biggest differences versus a passive Canadian REIT ETF is its willingness to move outside the benchmark. While funds like XRE remain almost entirely tied to the domestic market, MREL has meaningful international exposure. As of April 30, 2026, approximately 23.8% of the portfolio was invested in U.S. real estate securities.

Sector positioning is also noticeably different. Relative to XRE, MREL was underweight retail, multifamily residential, and industrial REITs while maintaining a larger allocation to healthcare real estate. The U.S. allocation has also given the fund exposure to areas that Canadian REIT investors often miss entirely, including data centre REITs and homebuilders.

And then there is the income component. After all, MREL is ultimately designed as an income-oriented strategy. The ETF currently pays a monthly distribution of $0.075 per share. Based on recent market prices available through Wealthsimple, that works out to an annualized yield of roughly 6.7%.

So, if your primary objective is monthly income while still maintaining competitive long-term returns, at least relative to the Canadian REIT ETF universe, MREL has historically done a very good job of delivering.

MREL: The Bad

You would think that a portfolio comprised largely of Canadian real estate investment trusts would have fairly decent liquidity. No, Canada is not the United States when it comes to trading volumes, but many of the underlying REITs themselves trade actively and often with relatively tight bid-ask spreads.

Since ETF liquidity is ultimately derived from the liquidity of the underlying holdings and the creation-redemption mechanism, you would expect that to translate into reasonably efficient trading for MREL as well. Well, that is where things start to get a little frustrating.

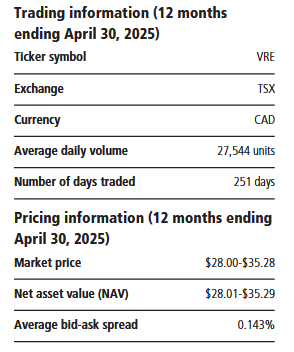

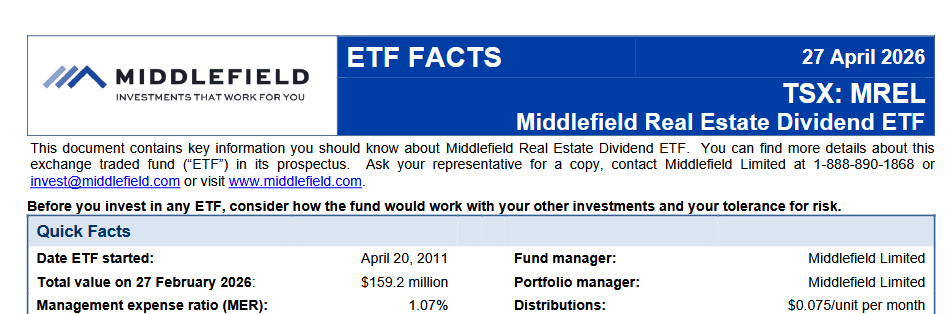

Looking at MREL's ETF Facts document dated April 27, 2026, Middlefield discloses an average bid-ask spread of 0.47% over the 12-month period ending February 27, 2026. Holy crap, that is wide.

Source: Middlefield

For investors unfamiliar with the concept, the bid is the price buyers are willing to pay, while the ask is the price sellers are willing to accept. The difference between the two represents an implicit trading cost. The wider the spread, the more friction exists when entering or exiting a position.

A long-term investor collecting monthly distributions probably won't lose much sleep over a one-time trading cost. But it still matters. Investors who regularly add to positions, reinvest distributions, use fractional-share purchases, or rebalance portfolios periodically are all exposed to that spread. Wider spreads generally mean worse execution.

To put this into perspective, let's compare MREL against another Canadian REIT ETF. The Vanguard FTSE Canadian Capped REIT Index ETF (VRE) reported an average bid-ask spread of 0.143% for the 12-month period ending April 2025 according to its ETF Facts document.

Source: Vanguard

That's not spectacular by U.S. ETF standards, but it is perfectly reasonable for a Canadian niche-sector ETF. MREL's 0.47% spread is more than three times wider. That difference is large enough that it becomes difficult to ignore.

What's particularly puzzling is that I don't think this is a Canadian REIT problem. The underlying securities themselves are generally liquid enough. Nor is this a tiny ETF with only a few million dollars in assets. MREL manages approximately $164 million, which should be sufficient to support tighter secondary market trading.

My suspicion is that the issue comes down to market-making activity, trading volumes, or how aggressively authorized participants are arbitraging price discrepancies between the ETF and its underlying holdings. Whatever the explanation, the end result is the same: investors are paying a noticeably larger trading cost than they probably should be.

And that is unfortunate because it detracts from what is otherwise a strong product. This is one area where I think Middlefield's trading and teams should focus their attention. For many experienced ETF investors, a persistently wide bid-ask spread can absolutely become a deciding factor when comparing otherwise similar funds.

MREL: The Ugly

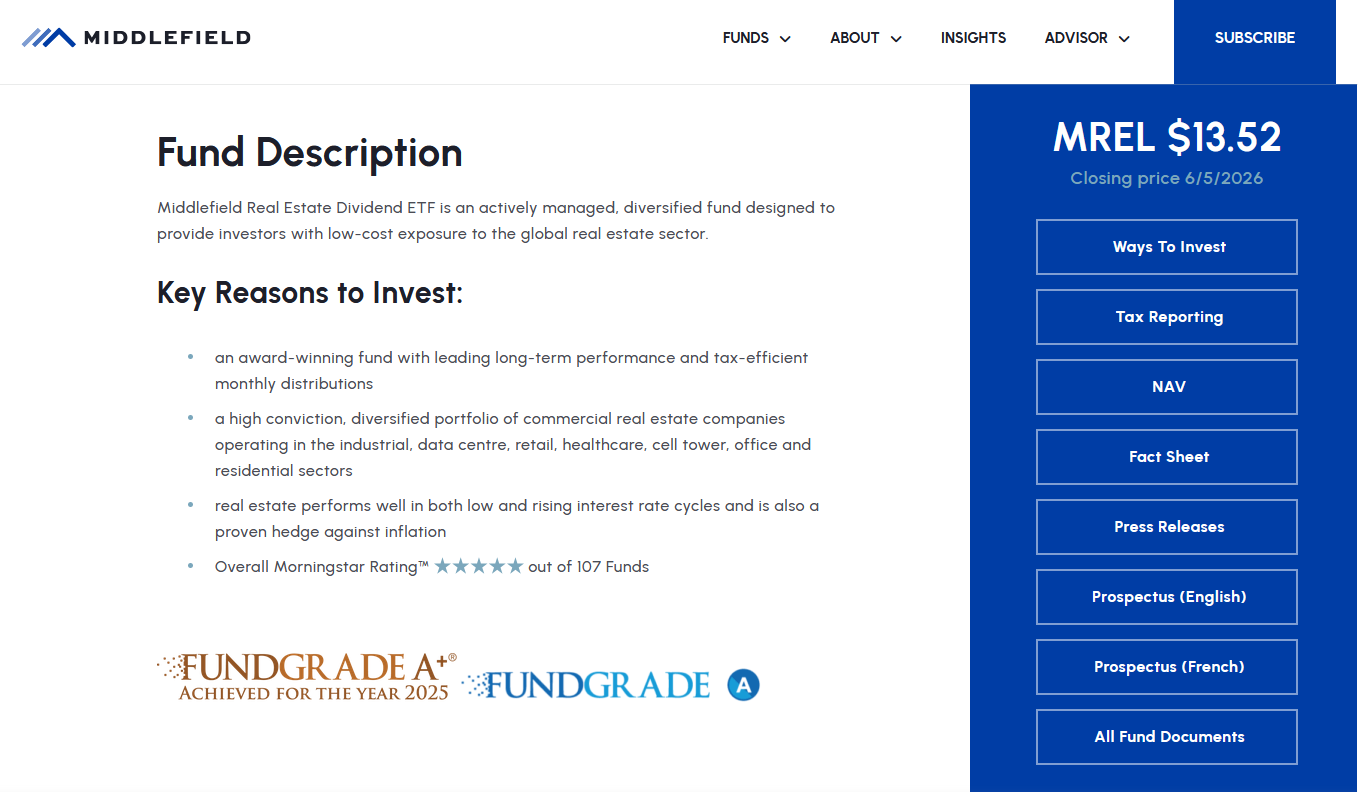

This is where I'm going to take the kiddie gloves off and really say what's on my mind. If you visit MREL's homepage, one of the key reasons to invest highlighted by Middlefield is: “…an actively managed, diversified fund designed to provide investors with low-cost exposure to the global real estate sector.”

Source: Middlefield

Now, technically speaking, most of that statement is true. It is actively managed, it is diversified, it does provide exposure to global real estate. The part I struggle with is the "low-cost" claim.

Look, I understand active management costs more than passive indexing. I'm perfectly willing to accept that. Research teams cost money, portfolio managers cost money, trading costs money. If an active manager can demonstrate value, paying somewhat higher fees can be justified.

But not at the level MREL is charging. If you look at the headline number on the fund's homepage, you'll see a management fee of 0.75%. On the surface, that looks reasonable. The problem is that the management fee is not the same thing as the management expense ratio (MER).

Source: Middlefield

To find the actual MER, I had to leave the homepage, navigate into the fund documents section, locate the regulatory filings, and then download the ETF Facts document dated April 27, 2026. Only then do we discover that MREL's actual management expense ratio is 1.07% as of February 27, 2026.

Source: Middlefield

Holy crap. To put that into perspective, the passive competitors we discussed earlier aren't even close. XRE and ZRE carry MERs of 0.6% and 0.61%, respectively. VRE is cheaper still at just 0.39%. MREL, meanwhile, sits at 1.07%. That's very expensive, coming close to leveraged ETF MERs.

And what bothers me isn't necessarily that the ETF charges more. It's the fact that the fund’s homepage marketing emphasizes "low cost" with a 0.75% management fee, while the actual 1.07% MER requires several extra clicks and a separate regulatory document to uncover.

Now, to be completely fair, we need to acknowledge something important: the outperformance discussed earlier was achieved after all of these costs were deducted. The higher fees, operating expenses, administrative expenses and trading costs were already reflected in MREL's returns.

Despite that handicap, the fund still managed to outperform both XRE and ZRE over the period examined. That deserves recognition. But past outperformance does not guarantee future outperformance. Fees, on the other hand, are guaranteed. They show up every year, compound negatively every year, and act as a headwind every year.

Maybe Dean Orrico and his team continue to earn that fee, maybe they don't. As an investor, that's ultimately the bet you're making when you buy MREL. You're betting that Middlefield's active management can continue generating enough excess return to overcome one of the highest cost structures in the Canadian REIT ETF space.