COMX: A Diversified Approach to Commodity Producer Equities

Last Updated:

Do you remember when oil prices went negative? It was a demand shock. During COVID-19, global mobility collapsed almost overnight. Flights were grounded, supply chains stalled, and storage filled up. At one point in April 2020, futures prices for West Texas Intermediate crude briefly traded below zero as producers ran out of places to put excess supply.

Commodity producers felt that impact directly. These are the companies that extract, refine, and transport raw materials, and they were among the hardest hit during that period. Revenues fell, margins compressed, and capital spending was cut across the sector. By the end of 2020, the MSCI World Commodity Producers Index had fallen -15.10%, while the MSCI World Index rallied 15.9%.

But market regimes change. In the years since, a number of factors has shifted the backdrop. Government spending during COVID supported demand, but it also contributed to a sharp rise in inflation. That, in turn, pushed commodities back into focus as a store of value and a source of pricing power.

Then came supply-side shocks. Russia’s invasion of Ukraine in 2022 disrupted global energy and agricultural markets. Sanctions and export restrictions tightened supply across oil, natural gas, and key inputs like fertilizers and grains. Unsurprisingly, commodities performed well, with the MSCI World Commodity Producers Index returning 32.13% in 2022 while the MSCI World Index fell -18.14%.

More recently, conflicts involving the U.S., Israel, and Iran have added pressure to global energy markets, particularly through disruptions in the Strait of Hormuz, a key shipping route and chokepoint that handles roughly one-fifth of global oil flows. As a result, commodities and commodity-linked equities have been among the stronger-performing areas of the market in recent years.

That raises a practical question, though: how can the average person actually invest in commodities? Some are straightforward. Precious metals like gold and silver can be purchased directly and held.

But that approach doesn’t translate well across the entire commodity spectrum. You cannot realistically store barrels of oil or bushels of wheat. Even when exposure is available through futures markets, it introduces complexity and higher fees.

This creates an access problem. Commodities can offer diversification benefits due to their historically low correlation with traditional asset classes, but they are not always easy to hold in a portfolio.

One way around that is through equities. Instead of owning the commodity itself, investors can gain exposure through the publicly traded companies that explore and extract it, and for Canadian investors, the newly launched Global X All-In-One Commodity Producers Equity ETF (COMX) is worth a look.

What is a Commodity?

A commodity is a raw material. It is something that can be produced, extracted, and traded in large quantities, often with little differentiation between one unit and another.

The defining characteristic of commodities is their fungibility. A barrel of oil or a ton of copper is generally interchangeable with another of the same grade, regardless of where it was produced. That standardization is what allows commodities to be traded globally with transparent pricing.

Whether you realize it or not, you interact with commodities every day. The gasoline in your car comes from crude oil. The wiring in your home relies on copper. The food you eat depends on agricultural inputs like wheat, corn, and fertilizers. Even the rubber in your sneakers and the plastics in everyday goods trace back to petroleum-based commodities.

Because of this, commodities sit at the foundation of global trade. They are not end products. They are inputs. Energy powers transportation and manufacturing. Metals go into construction, electronics, and infrastructure. Agricultural commodities feed populations and supply food chains. This makes them deeply embedded in the global economy.

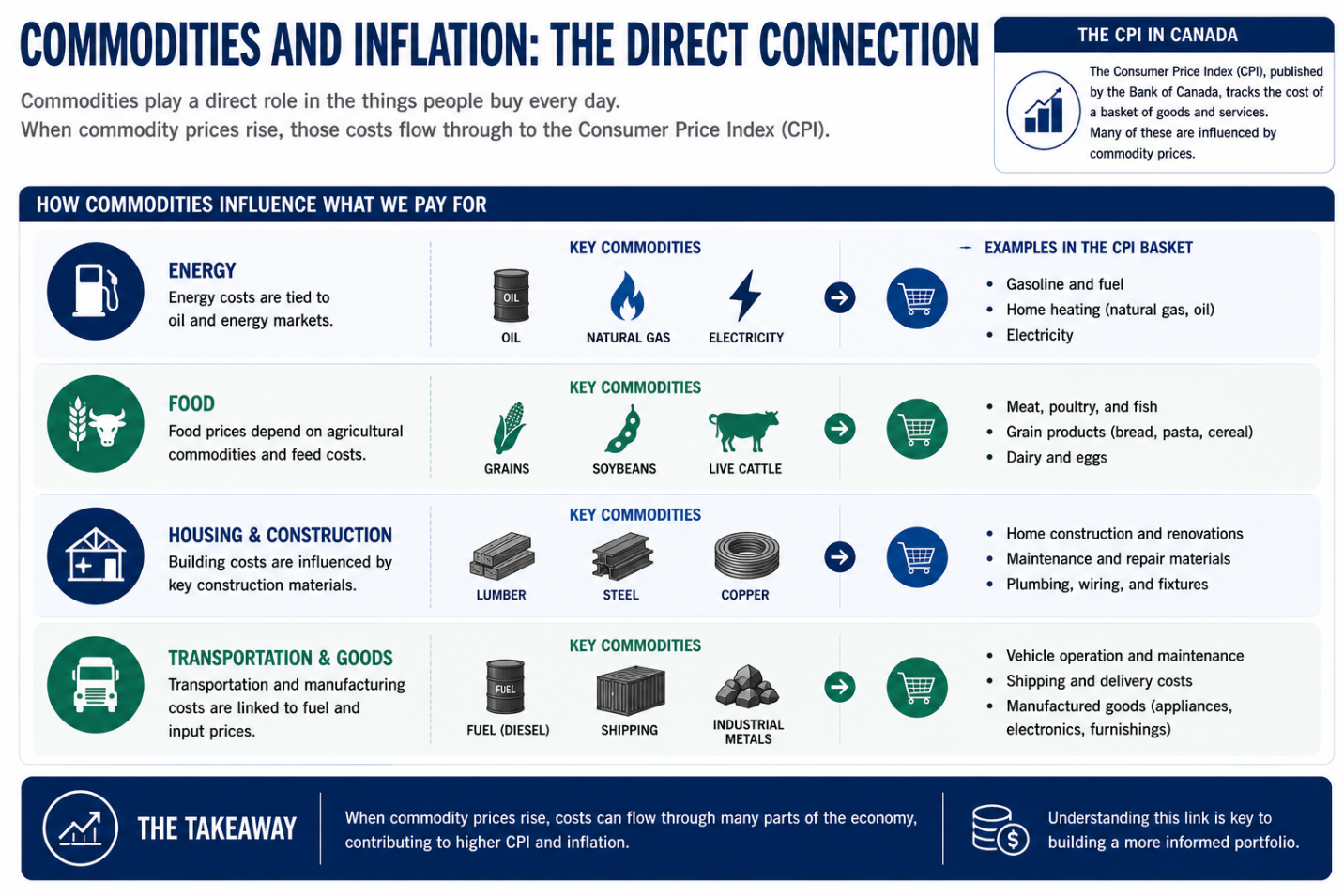

That role also ties commodities directly to inflation. For Canadian investors, one of the most widely followed measures is the Consumer Price Index (CPI), published by the Bank of Canada. The CPI tracks the cost of a basket of goods and services, many of which are directly or indirectly influenced by commodity prices. For example:

- Energy: gasoline, natural gas, and electricity costs are tied to oil and energy markets.

- Food: prices for meat, grains, and dairy depend on agricultural commodities and feed costs.

- Housing and construction: materials like lumber, steel, and copper influence building costs.

- Transportation and goods: shipping and manufacturing costs are linked to fuel and input prices.

Source: Bank of Canada as of May 12th, 2022.

When commodity prices rise, those increases tend to filter through to the broader economy, contributing to higher inflation readings. Commodity exposure has historically been viewed by some investors as a potential inflation-sensitive allocation.

The Benefits of a Commodities Allocation

Equities are primarily driven by factors such as earnings growth, share buybacks, and dividends. Over time, stock returns reflect the ability of companies to generate and grow profits. Bonds, on the other hand, are influenced by interest rates, credit conditions, and income from fixed coupon payments.

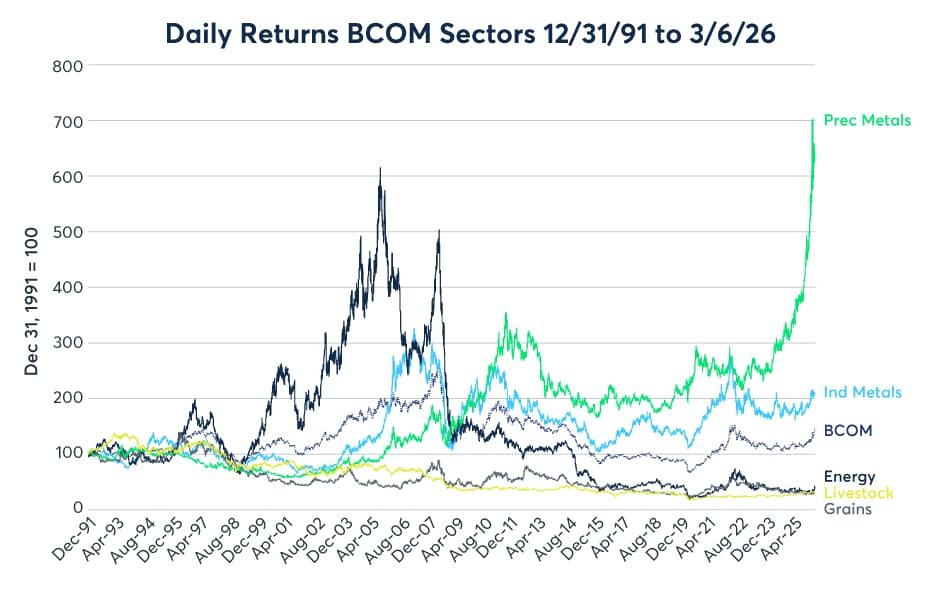

Commodities operate on a different set of drivers. Their prices are determined largely by supply and demand. Production levels, geopolitical disruptions, weather patterns, inventory levels, and transportation constraints all play a role.

Source: CME Group as of March 17, 2026.

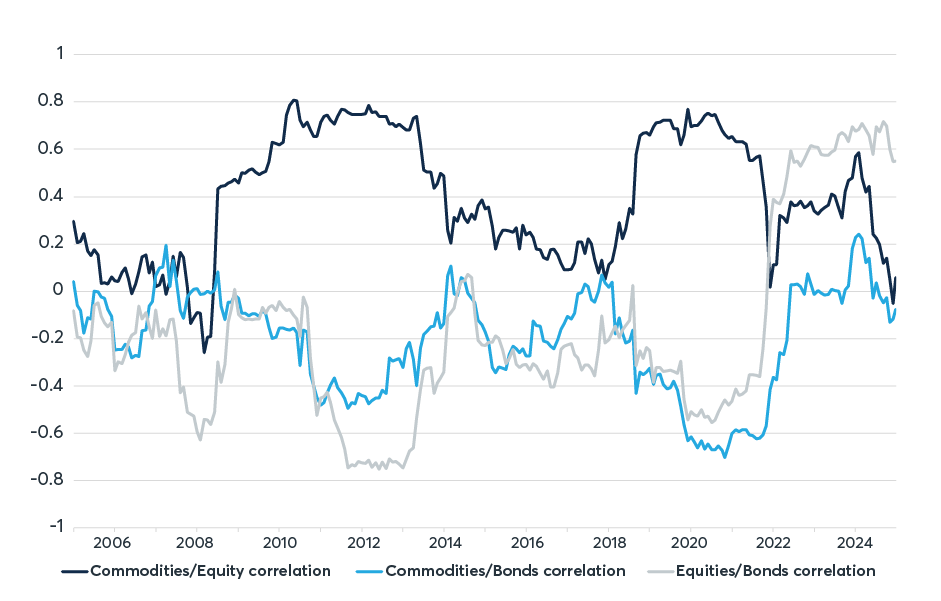

Because of these differences, commodities tend to have lower correlation with stocks and bonds. When traditional assets are moving in one direction, commodities may not follow the same path.

Source: CME Group as of May 21st, 2025.

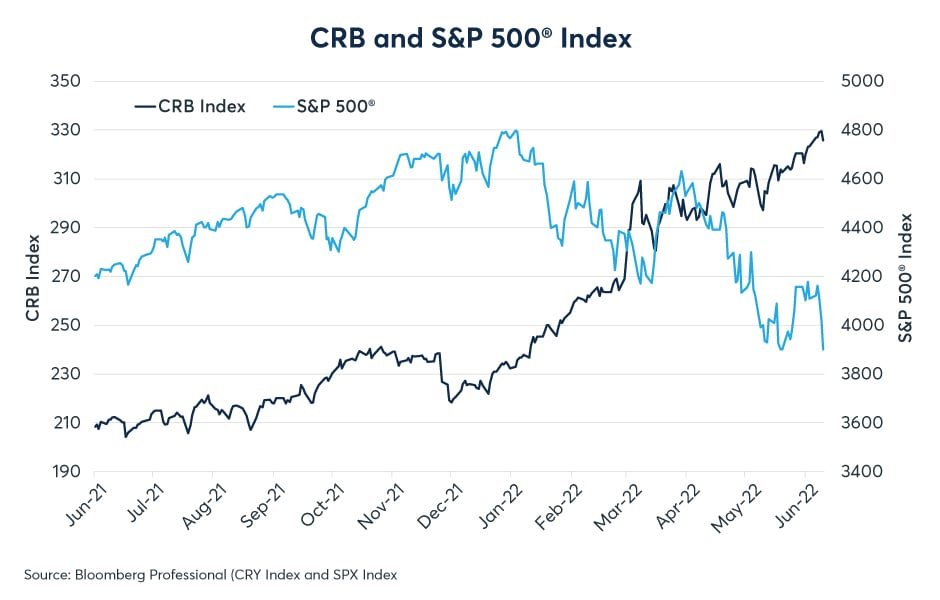

A recent example is 2022, when both stocks and bonds declined in response to rising interest rates and elevated inflation. During that same period, commodities benefited from the inflationary environment and supply disruptions, highlighting their different behavior within a portfolio.

Source: CME Group as of June 22, 2022.

That distinction is what underpins their role in diversification. Commodities can be volatile, but because they are driven by different factors, they can provide balance when combined with other asset classes.

For investors, incorporating a commodity allocation and rebalancing may behave differently from traditional asset classes within a portfolio, particularly in macro environments where inflation and supply shocks play a larger role.

The Different Ways to Invest in Commodities

As noted earlier, some commodities can be owned directly. The most straightforward examples are metals. Precious metals like gold and silver are commonly held physically, but even base metals such as copper or iron could, in theory, be stored if you had the space and inclination.

That said, most commodities are far less practical to hold. Energy is the clearest example. Storing barrels of crude oil is not just inconvenient, but also involves transportation, storage infrastructure, environmental regulations, and likely local zoning issues.

The same applies to natural gas, which requires specialized containment, or agricultural commodities like wheat or corn, which are perishable. For most investors, the closest they come to owning these commodities directly is the gasoline in their car or the food in their fridge.

Because of these constraints, financial markets have developed alternative ways to access commodities. The most common is through derivatives, specifically futures contracts.

A futures contract is an agreement to buy or sell a commodity at a specified price on a set date. These contracts “derive” their value from expectations about where prices will be at that point in time. They are widely used by both producers and investors.

Importantly, futures do not track spot prices perfectly. For example, if you buy a crude oil futures contract expiring in August 2026, its price will be influenced by expectations about supply, demand, storage costs, and interest rates over that period. While it may be highly correlated with the current or “spot” price of oil, the relationship is not one-to-one.

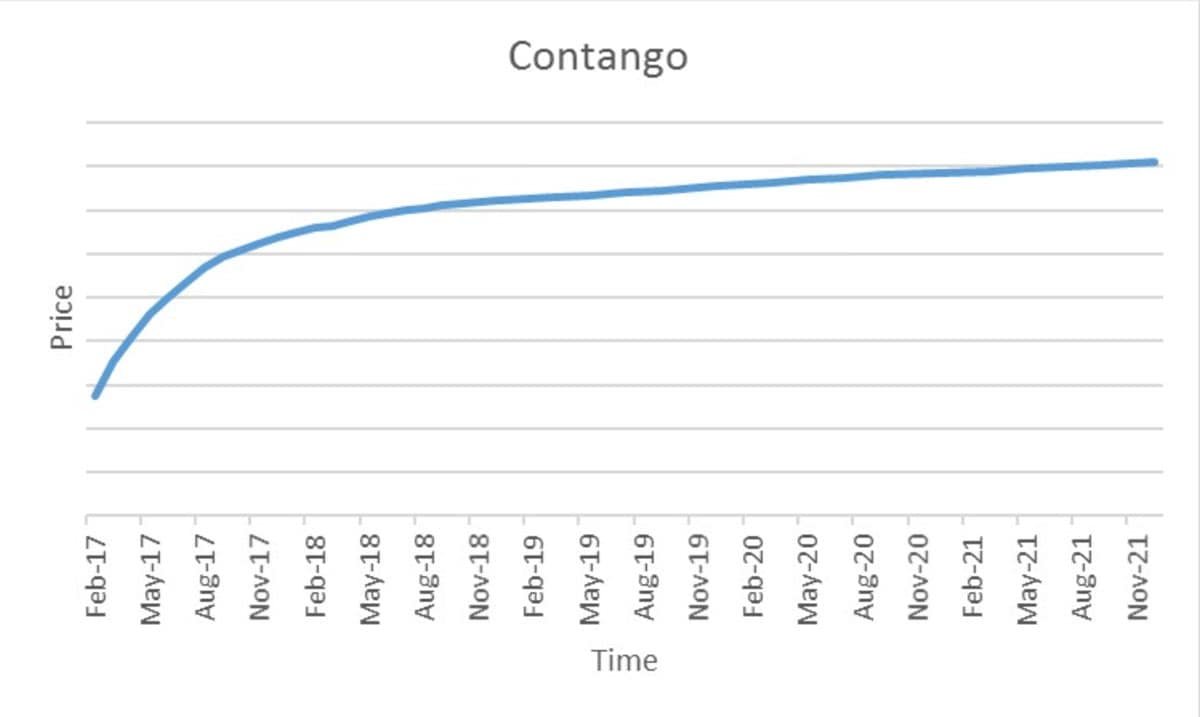

This leads to one of the key challenges in commodity investing through futures: contango. Contango refers to a situation where futures prices for later delivery dates are higher than near-term prices. When plotted on a curve, prices slope upward over time. This is common in commodities due to storage costs, insurance, financing, and the general expectation that carrying a commodity forward in time has a cost.

Source: CME Group as of May 5th, 2026.

The issue arises because futures contracts expire. If you want to maintain commodity exposure, you cannot simply hold one contract indefinitely. You must “roll” it, or be prepared to take physical delivery. Rolling means selling the expiring contract and buying a new one with a later maturity.

In a contango market, this can create a drag on returns, called “negative roll yield”. You are effectively selling the nearer-term contract at a lower price and buying the longer-dated contract at a higher price. Repeating this process over time can erode performance, even if the underlying commodity price is stable. For investors, this can potentially reduce the diversification benefits of a commodity allocation.

How Commodity Producer Equities Can Help

A third approach is to invest in the companies that produce commodities. These include energy companies involved in oil and gas extraction, metals and mining firms producing copper, iron ore, or lithium, and agricultural businesses tied to fertilizers and crop production.

Canadian investors are likely familiar with many of these names, but large producer markets also exist in the United States and globally, particularly in resource-rich regions such as Australia.

Commodities themselves do not generate cash flow, but producers do. They sell output, generate earnings, and can return capital through dividends, reinvest in expansion, or repurchase shares. This introduces the potential for long-term growth beyond the speculation and supply/demand mechanics that drive raw commodities.

This approach does come with trade-offs though. Commodity producers are still equities. Their share prices can be influenced by broader market movements, interest rates, and company-specific factors. At the same time, they retain sensitivity to underlying commodity prices. When prices rise, revenues and margins often improve, but falling commodity prices like during COVID can hurt them.

Moreover, company-specific risks remain. In particular, operational issues, such as accidents or environmental incidents, can detract from performance. Political and regulatory risks can also play a role, particularly for assets located in emerging markets, where nationalization or expropriation is a possibility.

A Diversified Approach to Commodity Producers

Diversification becomes important in this context. Holding a range of producers across commodities, geographies, and business models can help reduce exposure to any single risk. This is where a more diversified vehicle like the Global X All-In-One Commodity Producers Equity ETF (COMX) may be useful.

COMX uses “ETF of ETFs” structure to provide exposure to a global set of commodity producers. The portfolio maintains a 100% equity allocation, with rebalancing handled at the manager’s discretion. Foreign currency exposure is not hedged back to the Canadian dollar.

For investors reliant on passive global equity benchmarks, COMX may provide additional exposure to sectors that are less represented in broad equity benchmarks. Broad indices such as the MSCI World typically have relatively low exposure to commodity-oriented sectors like energy and materials, often in the low single digits. An allocation to an ETF like COMX can therefore be used to increase exposure to those areas more directly to position against inflation.

Source: MSCI as of April 30th, 2026.

For investors with different objectives, COMX also has two companion ETFs worth keeping in mind:

- The Global X All-In-One Commodity Producers Equity Covered Call ETF (CMCC) introduces an options overlay, selling covered calls on up to 50% of the portfolio to generate income at the expense of some upside participation.

- The Global X Enhanced All-In-One Commodity Producers Equity Covered Call ETF (CMCL) applies a similar strategy with a modest level of leverage, targeting approximately 1.25x, or 125% notional exposure through cash borrowing.

Across these structures, the underlying idea is consistent. Commodity exposure can be accessed in different ways, each with its own trade-offs between simplicity, income, and risk. COMX charges a 0.55% management fee, while CMCC and CMCL charge 0.65% and 0.85%, respectively.

Regardless of whether the approach is core equity exposure through COMX, income-focused through CMCC, or enhanced through CMCL, the starting point remains the same: commodities are a distinct asset class, and how you access them can meaningfully influence outcomes.