The Charles Schwab Quadfecta ETF Portfolio

Last Updated:

Rick Ferri, a well-respected Chartered Financial Analyst (CFA), retired Marine Corp fighter pilot, and a staunch advocate of index investing, is a figure I hold in high regard. He's not only a Boglehead and a prolific author but also hosts a podcast and runs an advice-only investment advisory.

One of his standout contributions to retail investors is the creation of the Core-4 Portfolios. In his words: “The idea was to provide a simple, tax-efficient, broadly diversified portfolio of only four low-cost index funds and ETFs.”

The original Core-4 includes a total US stock market index fund, an international stock index fund, a US bond index fund, and a Treasury inflation-protected securities fund (TIPs).

While Core-Four is trademarked, I've put a twist on Ferri’s model with what I call the "Quadfecta" portfolio. This variation swaps the international equities for REITs, aligning more with my personal investment preferences and views on diversification.

Here’s how you can adapt this model to build your “Quadfecta” portfolio using some of Charles Schwab's low-cost index ETFs.

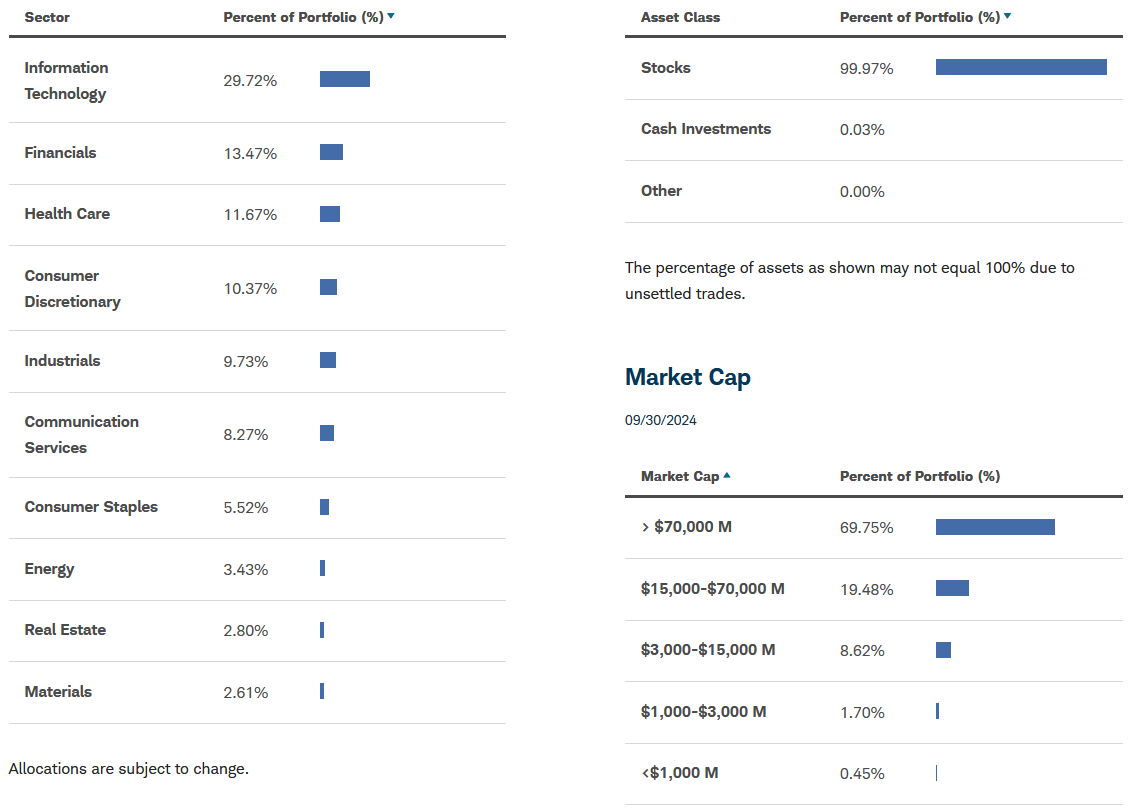

Schwab U.S. Broad Market ETF (SCHB)

Allocating a substantial 60% of our Quadfecta portfolio to U.S. equities, my aim is to harness the equity risk premium as cost-effectively as possible.

This involves capturing the entire spectrum of the market—small, mid, and large-cap stocks across all sectors—through a market-cap weighted approach for efficiency.

SCHB perfectly fits this strategy by tracking the Dow Jones U.S. Broad Stock Market Index, which represents the 2,500 largest U.S. equities.

Its market-cap weighting leads to an impressively low annual turnover of just 3.33%, minimizing return drags and enhancing tax efficiency.

SCHB is a stalwart in the ETF world, managing $31 billion in assets. What seals the deal for me is its incredibly low expense ratio of 0.03%, making it an ideal cornerstone for our portfolio.

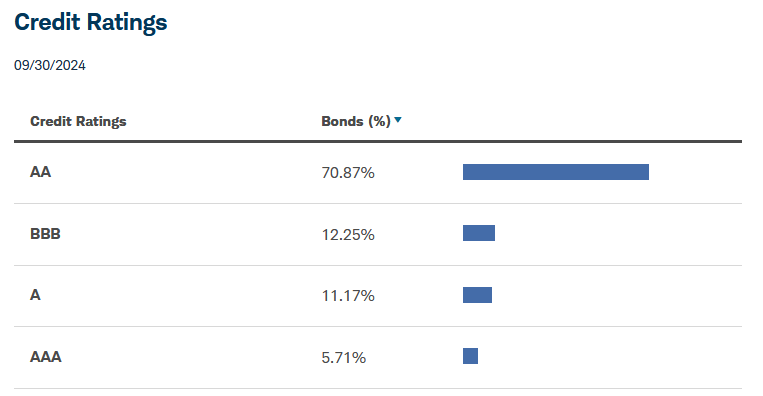

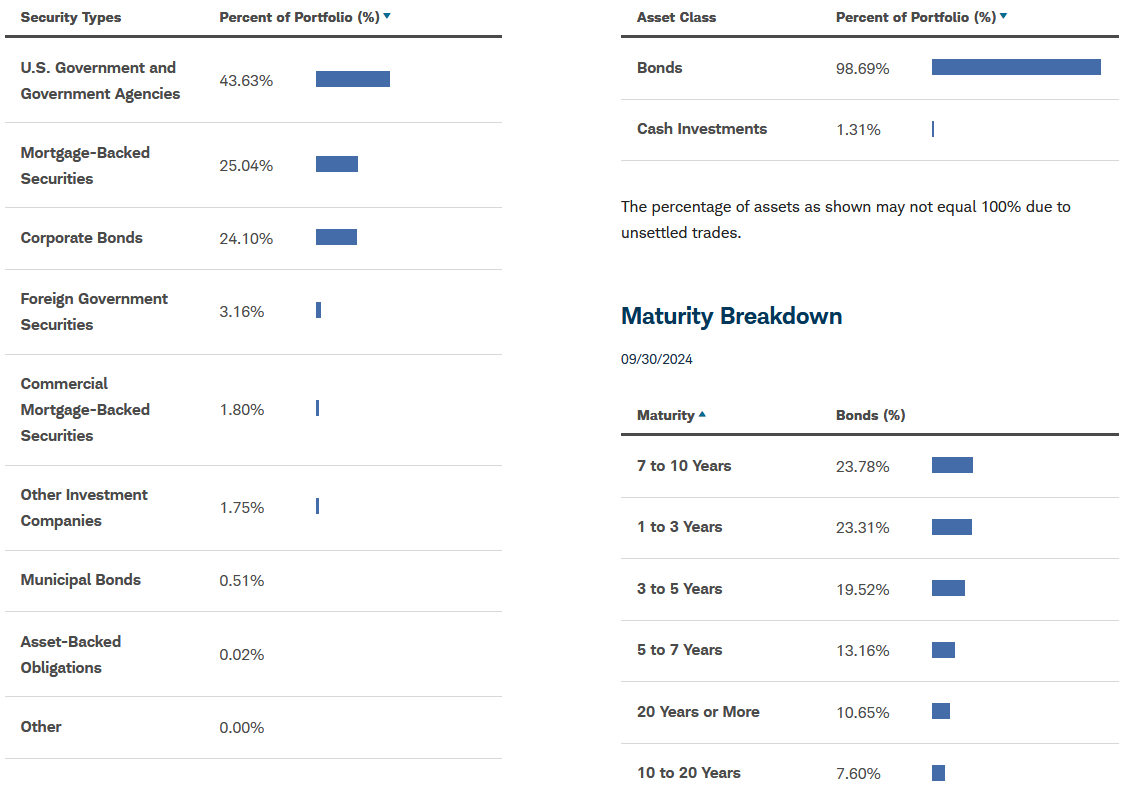

Schwab U.S. Aggregate Bond ETF (SCHZ)

The Quadfecta is meant to be a balanced portfolio, so I’m not using a 100% equity allocation. Instead, I'm looking for a more nuanced blend of risk and return with a 20% bond allocation. Bonds play a crucial role here, offering potentially uncorrelated returns to equities by tapping into different risk premiums—namely credit and maturity.

To achieve this, I turn to SCHZ for its affordability and broad exposure. This ETF tracks the Bloomberg U.S. Aggregate Bond Index, encompassing a diverse range of over 10,000 U.S. Treasuries, mortgage-backed securities (MBS), agency bonds, and investment-grade corporate bonds across multiple maturities.

SCHZ is a quintessential aggregate bond fund, featuring a 6.0-year duration and a 4.24% yield to maturity, positioning it as an ideal option for a wide range of investors. Its costs a 0.03% expense ratio.

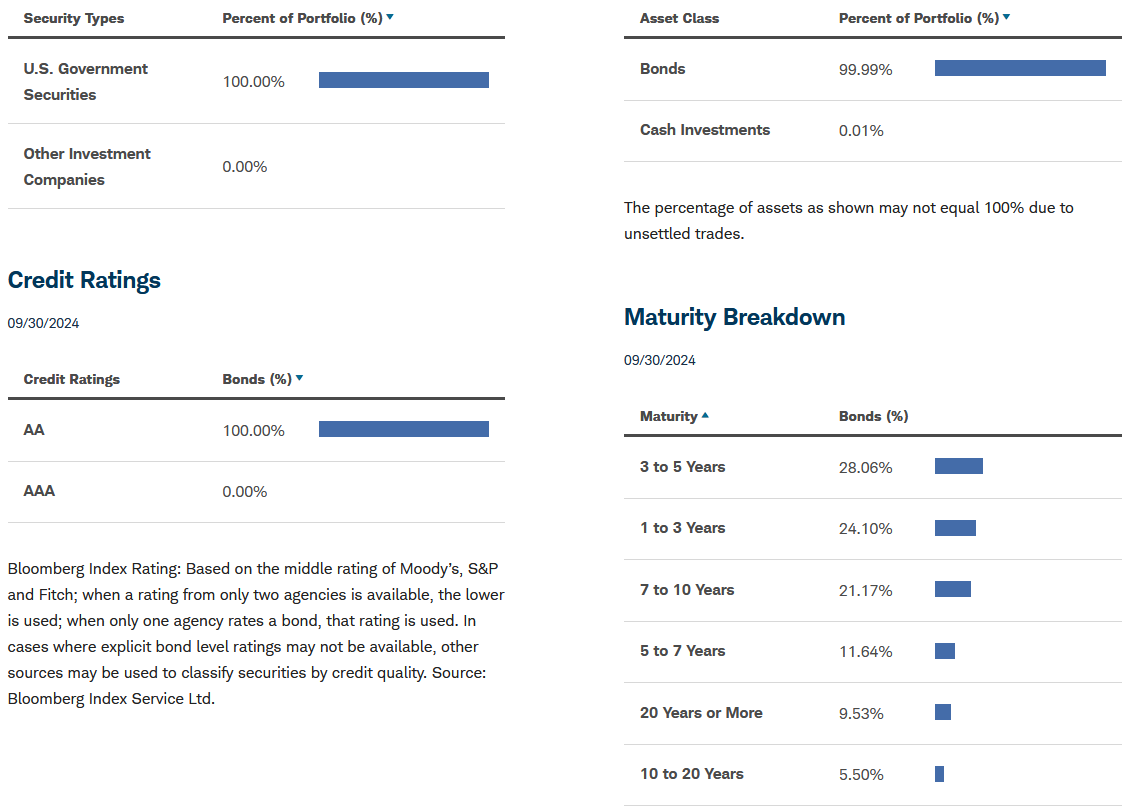

Schwab U.S. TIPS ETF (SCHP)

Despite the strengths of SCHZ, it has a notable weakness: inflation vulnerability. Nominal bonds generally underperform during inflationary periods because their fixed interest payments lose purchasing power as prices rise. This makes them less appealing during times of high inflation.

To hedge against inflation, I'm incorporating 10% TIPS into the Quadfecta. TIPS differ from regular bonds because they are indexed to the Consumer Price Index (CPI), meaning the principal and thus the interest payments adjust in line with inflation.

For those looking to include TIPS in their investment strategy, SCHP is an excellent vehicle. This ETF tracks the Bloomberg U.S. Treasury Inflation-Linked Bond Index, offering a broad exposure to U.S. inflation-protected bonds.

With a current duration of 6.8 years and an average yield to maturity of 3.71%, SCHP not only provides a safeguard against inflation but does so at a very low cost, featuring an expense ratio of just 0.03%.

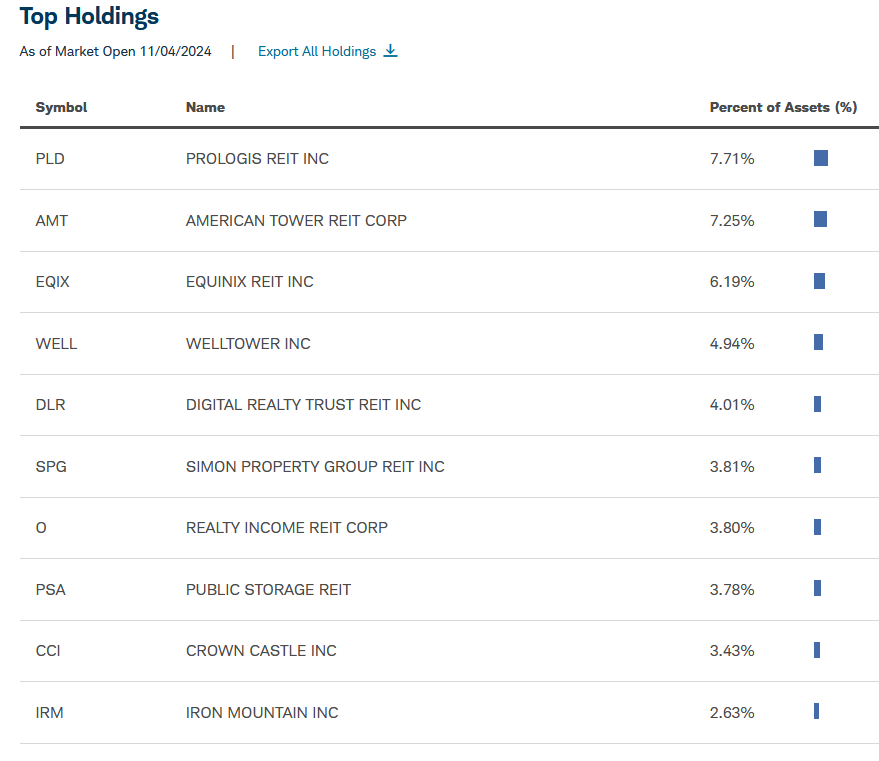

Schwab U.S. REIT ETF (SCHH)

The final component of the Quadfecta portfolio is 10% exposure to real estate, which I value for its potential to deliver returns that are not perfectly correlated with the stock market.

Real estate is influenced by different economic drivers such as interest rates, demographics, and consumer behavior, making it a useful diversification tool.

However, direct investment in real estate comes with its own set of challenges. Physical properties are not only illiquid, meaning they can't be quickly sold for cash, but they also involve maintenance costs, property taxes, and potential mortgage interest expenses.

An efficient way to gain exposure to real estate without these drawbacks is through Real Estate Investment Trusts (REITs), and SCHH is an ideal ETF for this purpose.

It tracks the Dow Jones Equity All REIT Capped Index, which includes around 120 equity REITs. This ensures you're invested in a broad array of real estate sectors, including residential, healthcare, cell towers, data centers, warehouses, self-storage, office, retail, and hospitality.

SCHH comes with a reasonable expense ratio of 0.07% and offers a higher income potential with a 30-day SEC yield of 3.62%. However, due to its distribution characteristics, it's most tax-efficient when held in a tax-sheltered account like an IRA.

Putting it all together

A balanced allocation of 60% SCHB, 20% SCHZ, 10% SCHP, and 10% SCHH gives you a diversified portfolio composed of 60% U.S. equities, 20% aggregate bonds, 10% TIPS, and 10% real estate.

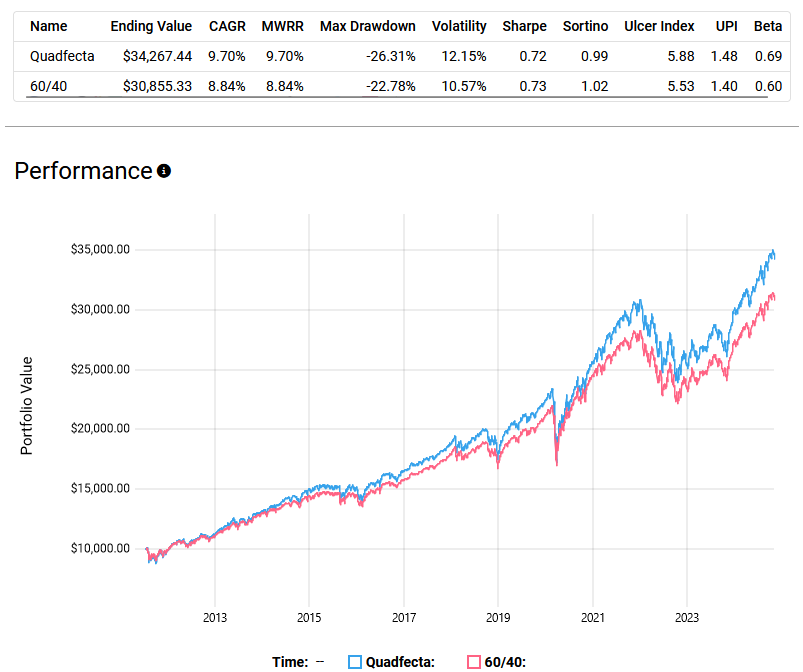

When we compare this “Quadfecta” setup with a more conventional 60/40 U.S. stock and bond portfolio, the results are impressive.

From July 2011 through November 2024, the Quadfecta portfolio (rebalanced quarterly) delivered a 9.7% annualized return (CAGR), outpacing the traditional 60/40 allocation, which returned 8.84% over the same period.

Risk-adjusted returns are also comparable: the Quadfecta portfolio has a Sharpe ratio of 0.72 versus 0.73 for the 60/40 portfolio. The Quadfecta was somewhat more volatile, showing a higher maximum drawdown and standard deviation due to its 10% lower bond allocation.

However, I still prefer the Quadfecta for its simplicity, easy rebalancing, and, above all, low costs. For this allocation, the weighted average expense ratio is a mere 0.034%, allowing you to keep more of your investment returns over the long term.