Amplify CWP Enhanced Dividend Income ETF (DIVO) Review

Last Updated:

There are plenty of ways to run a covered call ETF in 2025. The days of simply tracking a Cboe buy-write index are long gone. Today’s strategies involve everything from equity-linked notes and Section 1256 index contracts to the increasing use of single-stock and ETF-based options across a variety of strikes and durations.

That means the return profile, income potential, and overall risk of these strategies can vary widely. But as I always remind readers, the focus should be on total return, and ideally in a tax-efficient wrapper. Unfortunately, most covered call ETFs still fall short on that front. There are exceptions, though.

One ETF I’ve had on my radar for a while is the Amplify CWP Enhanced Dividend Income ETF (DIVO). It doesn’t always make headlines with flashy yields, so it tends to fly under the radar of income chasers. But I think that’s missing the forest for the trees. Here’s how DIVO stacks up in 2025.

DIVO: What I Like

What sets DIVO apart is that it’s a true actively managed strategy, not just on the stock selection side, but also in how it handles options.

The ETF doesn’t passively hug a benchmark or run the same systematic covered call overlays month after month. Instead, it takes a more hands-on, discretionary approach that adjusts with market conditions.

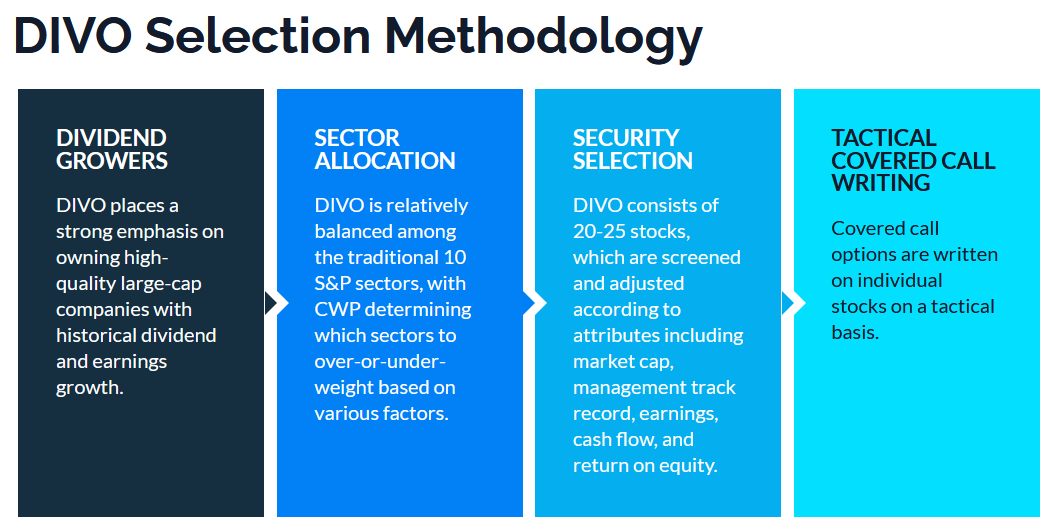

To really understand DIVO, it helps to think of it in two parts. First, there’s the core portfolio: a concentrated mix of 20 to 25 large-cap blue chip stocks drawn from across the GICS sectors (excluding real estate). This isn’t a closet index fund.

The subadvisor, Capital Wealth Planning (CWP), led by Kevin Simpson (you might’ve seen him on CNBC), builds the portfolio based on fundamental metrics like dividend growth, earnings momentum, return on equity, free cash flow generation, and overall management quality.

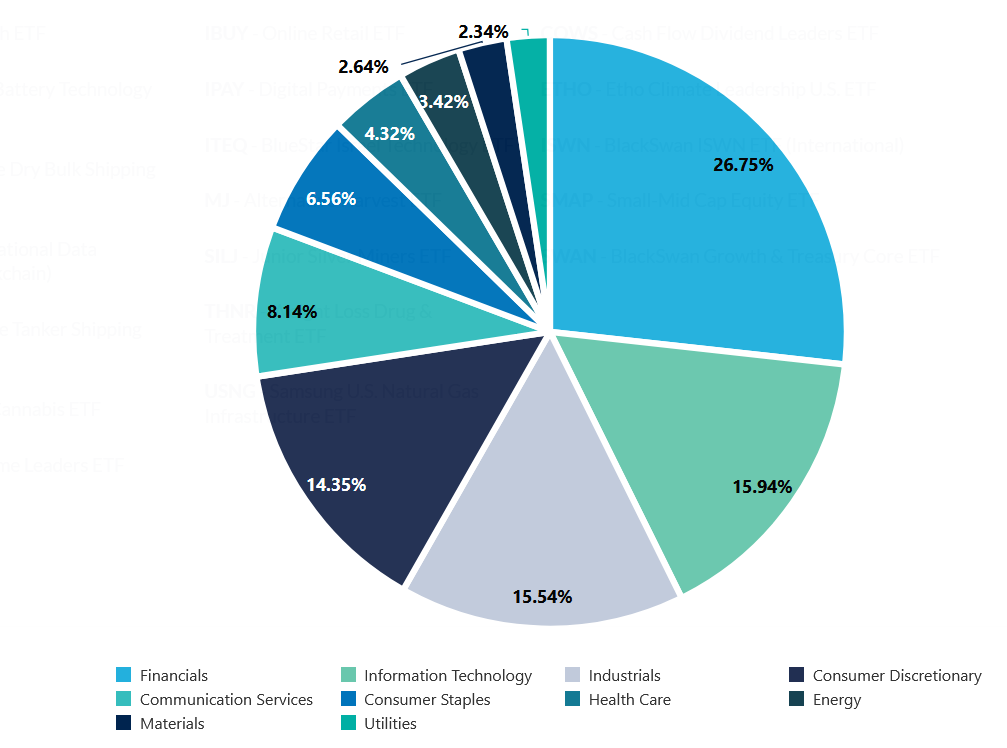

Sector weightings are tactical and reflect CWP’s macro-outlook. Right now, the portfolio leans more heavily on financials and industrials compared to the S&P 500.

The second component is the options overlay. Rather than writing calls on the entire portfolio or on an index, DIVO writes calls on individual names. This is done selectively and tactically. CWP considers factors like volatility, valuation, near-term catalysts, and technical levels before writing.

They also vary the strike prices and expiration dates rather than sticking to fixed rules. That flexibility helps preserve upside while still generating premium income.

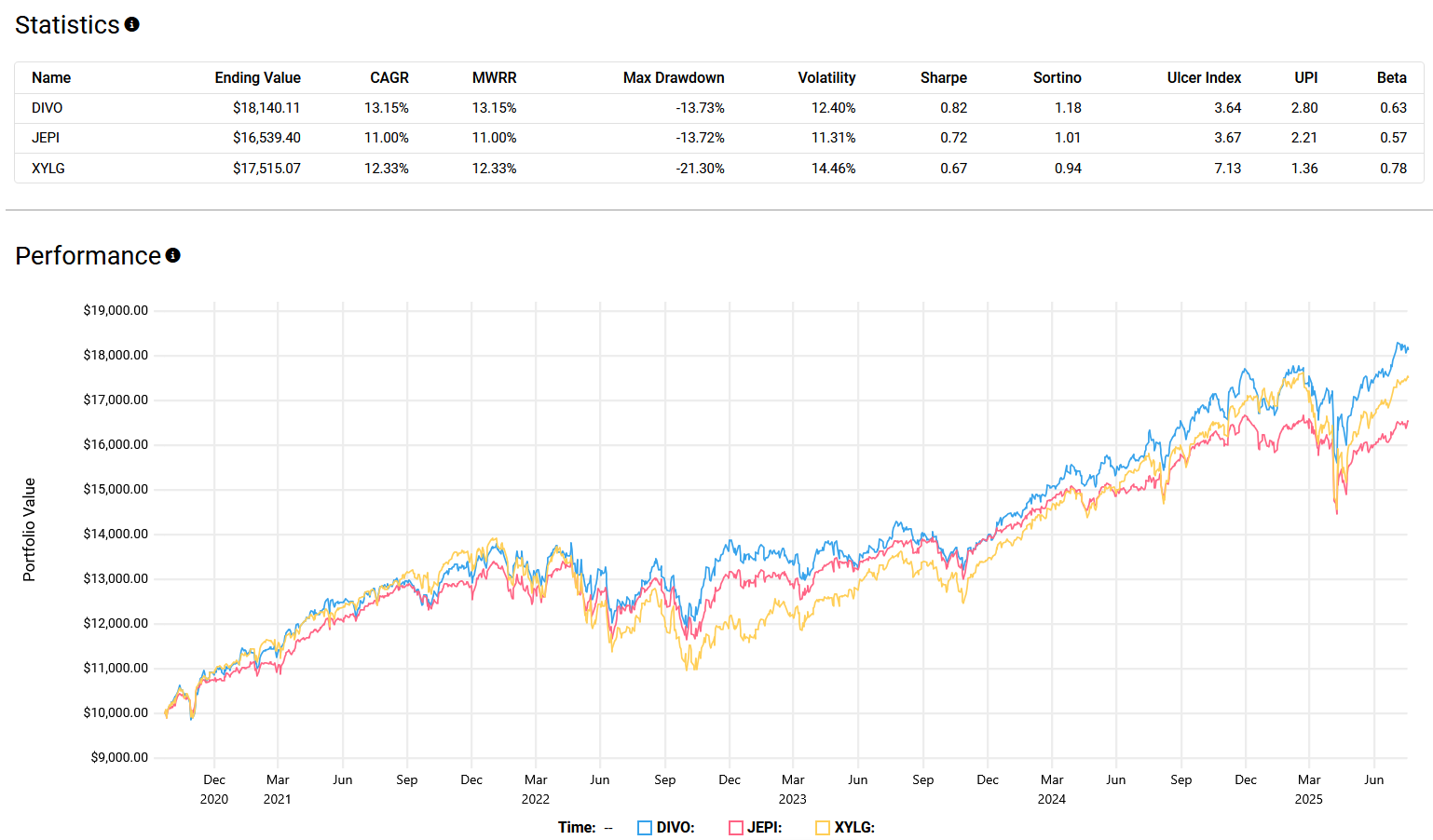

From September 21, 2020, through July 18, 2025, DIVO has outperformed popular large-cap covered call competitors like the JPMorgan Equity Premium Income ETF (JEPI) and the Global X Nasdaq 100 Covered Call & Growth ETF (QYLG), both on a total return and risk-adjusted basis.

Since its inception, it has returned 12.14% annualized, slightly lagging the S&P 500’s 14.42% total return but far outperforming the Cboe S&P 500 BuyWrite Index’s 6.43%.

DIVO: What I Dislike

No ETF is perfect, and DIVO has its fair share of drawbacks. Let’s skip the usual critique about diversification. If you’re buying DIVO, you’re probably not doing it to replicate a broad index. Complaining that it’s not the Vanguard Total Stock Market ETF (VTI) is missing the point. That’s just Boglehead brainwashing.

That said, the fee is hard to ignore. At 0.56%, it’s not egregious compared to some of the pricier Global X or NEOS covered call ETFs, but it’s not cheap either. JEPI charges 0.35%, and that’s quickly becoming the industry benchmark for actively managed covered call strategies. Goldman Sachs and other entrants are offering similar price points. In that context, DIVO looks a bit rich.

Yield also isn’t a headline grabber. While DIVO has held its own on a total return basis, most income-focused investors are drawn to covered call ETFs based on yield alone, often for the wrong reasons. With a distribution rate of 4.73%, DIVO pays more than your average dividend ETF but much less than the double-digit yields that dominate the category. That can be a tough sell to income chasers.

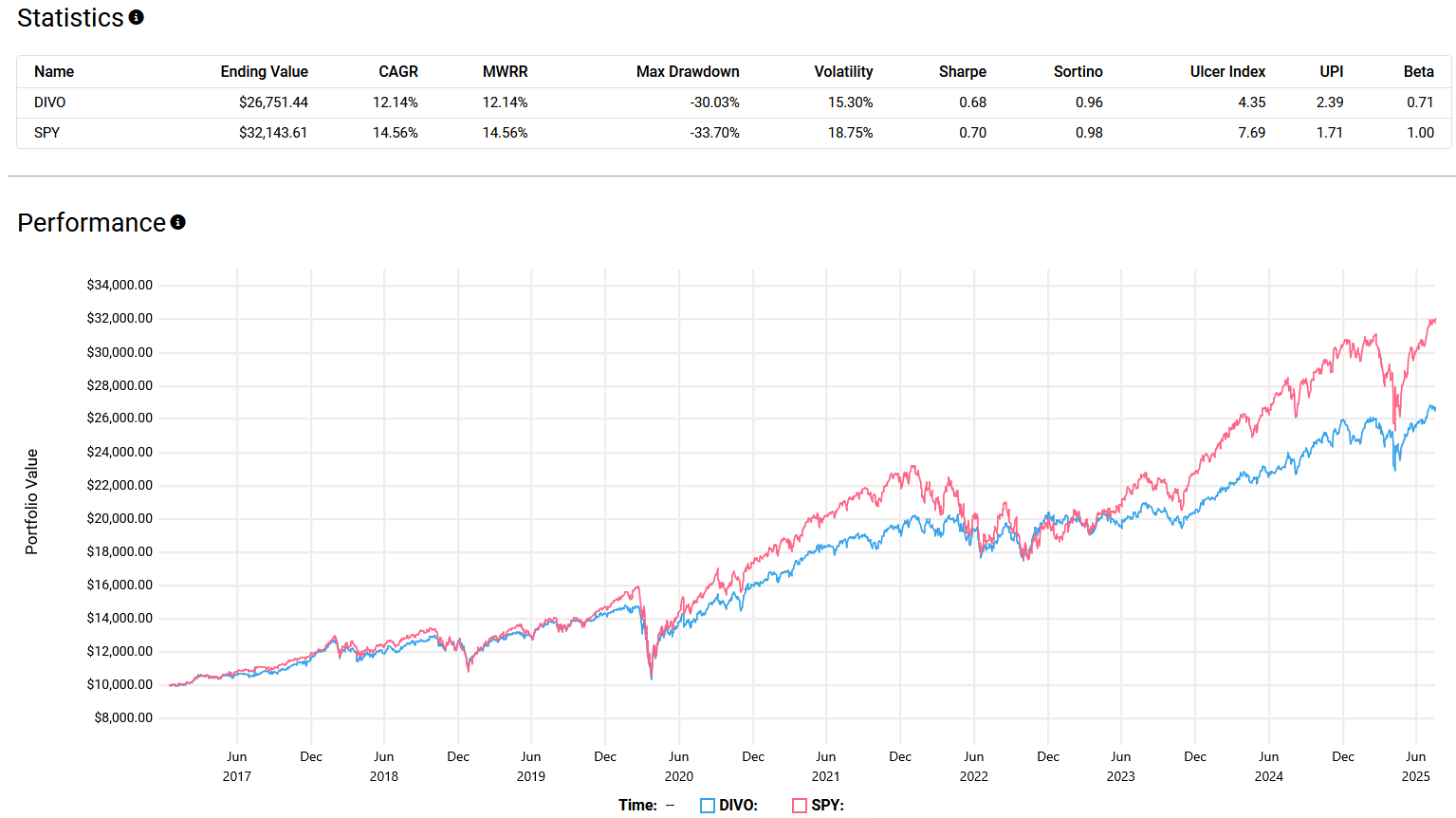

DIVO also may not be the best fit if your main goal is to generate the best total returns over stable, tax-efficient monthly income (70% of DIVO’s recent monthly distribution was estimated to be return of capital). On a total return basis, DIVO still lags the SPDR S&P 500 ETF Trust (SPY) from December 14, 2016, through July 17, 2025.

Its risk-adjusted performance comes much closer, which is impressive given that most covered call strategies cap upside without protecting downside. Credit there goes to CWP and Kevin Simpson’s experienced hand in navigating markets and delivering a decent Sharpe ratio.

But that leads to another issue: manager-specific risk. DIVO is tightly associated with CWP and Simpson’s decision-making. If something changes at the subadvisor level (philosophy, leadership, or execution) the fund’s future performance could look very different.

That kind of key-person dependence introduces style drift and succession risk over a long enough timeline, and investors should be aware of that before committing capital.

DIVO: My Verdict

I gave JEPI an 8/10 in my May 2025 review, and I think DIVO deserves a slight edge, so it’s an 8.5/10 from me. All in all, it’s what a covered call ETF should aspired to be like.

What I like about DIVO is its disciplined approach to active management. The high-conviction portfolio of blue-chip stocks gives it a strong core, while the selective, tactical call writing helps generate income without fully capping upside.

And the track record speaks for itself, outperforming most of its covered call peers on both return and risk-adjusted metrics. The fact that it’s done so without relying on extreme leverage or constant turnover adds to its appeal.

On the flip side, DIVO isn’t cheap. The 0.56% expense ratio is above what I’d like to see in a covered call ETF. The 4.7% distribution rate also won’t wow income chasers, even if the tax treatment is favorable.

And long-term, the reliance on Capital Wealth Planning and Kevin Simpson creates a real key-person risk. If the strategy or leadership changes, so could the fund’s performance profile. That’s something to watch closely.

In my opinion, DIVO is best suited for defensive-minded investors who are comfortable receiving a meaningful portion of their return as relatively tax-efficient income.

If you believe in the subadvisor’s active process and trust Kevin Simpson’s steady-handed strategy, I think DIVO is one of the better long-term covered call ETFs available in the U.S. market.